It’s early afternoon on an overcast Yukon day and CEO Peter Tallman is in show and tell mode at Lone Star, one of Klondike Gold’s properties in the heart of the historic Klondike goldfields. The geologist is dressed in old jeans, a flannel shirt, muddy gumboots and a baseball cap. The trip to the rugged property outside of Dawson City had Tallman’s pickup truck bouncing and bucking like an ornery bull with a rider on its back. It’s 3,000 kilometres and a world away from Vancouver’s Howe Street, a global centre for mining exploration finance.

The Lone Star mine was one of only a handful of bedrock gold mines in the Yukon, albeit a small-scale operation. The mine produced a small amount of gold at average grades of about 5.2 g/t Au between 1911 and 1914. Exhibit A is a faded wooden two-storey building, constructed in 1908 and visibly leaning. The building was abandoned circa World War 1, although it was reinforced and has been used since for various purposes. Nearby are high-grade surface and underground vein workings.

As Tallman walks through high grass toward the sun-burnt structure, he spots something and stops to pick it up. Exhibit B: a dilapidated shoe, several rusted metal tacks keeping the sole on. Tallman marvels at the resilience of the oldtimers, as he outlines his own plans to develop an economic gold deposit on the property.

“Imagine you’re working in minus 30 and wearing these on your feet,” he says, shaking his head.

Inside the dilapidated building are glimpses of the lengths to which fortune seekers would go – and the distances they would travel – in search of gold. After catching up on the news, the miners would line the walls with their newspapers – makeshift insulation in a land where winter temperatures routinely drop below -20 Celsius (-4 Fahrenheit). Posted alongside English-language newspapers from Winnipeg, Toronto and Montreal are broadsheets in Swedish and German.

In the Yukon, these bedrock miners were an anomaly. The Yukon Geological Society estimates that 20 million ounces of gold have been pulled from Klondike-area creeks and gravel beds since 1896. Virtually all of it, of course, has been alluvial gold. The lack of bedrock sources for the gold is one of the enduring riddles of the Yukon, where placer gold mining remains one of the largest industries. Several stores in Dawson City still accept gold nuggets as currency.

Tallman’s goal is to systematically explore the property and identify an open-pittable gold deposit of more than 1 million ounces, for starters. He joined Klondike Gold in December 2013. But before he got to the geology, Tallman spent most of the first year and a half cleaning up the corporate structure and rebuilding relationships in the Yukon. Predecessor companies had raised a lot of money, dug a trench that could be seen from space, and constructed some Cadillac core shacks. But little was spent on systematic property-wide exploration, and not much accomplished.

Diamond drilling is underway on this year’s 5,000- to 7,000-metre program. The 2018 exploration budget is $2.5 million, Klondike Gold’s largest yet, and work will include soil sampling and ground magnetics. The plan builds on last year’s exploration program ($2 million spent) and the Lone Star discovery of 2016, when Klondike spent $750,000 on exploration.

There is high-grade gold on the Lone Star property, as drill intercepts from both 2016 and 2017 have shown. They included:

– 2.4 g/t Au over 41 metres (Lone Star, 2017) – 2.4 g/t Au over 37 m (Lone Star, 2017) – 5.1 g/t Au over 14.3m (Nugget zone, 2016) – 3.3 g/t Au over 11.93m (Nugget zone, 2016)

But key to a new geological interpretation is the presence of disseminated lower-grade gold, which builds ounces even though it doesn’t generate sexy headlines. The new interpretation was the focus of a PhD thesis from Leeds geology student Matt Grimshaw, who will be back this summer helping SRK Consulting map the entire property. Tallman thinks as much as 90% of the gold in the Klondike could be disseminated.

Tallman has also brought on a VP Exploration to help him solve the geological riddles of the goldfields: Ian Perry. The geologist has more than 35 years of experience managing advanced exploration and development projects in Canada and internationally.

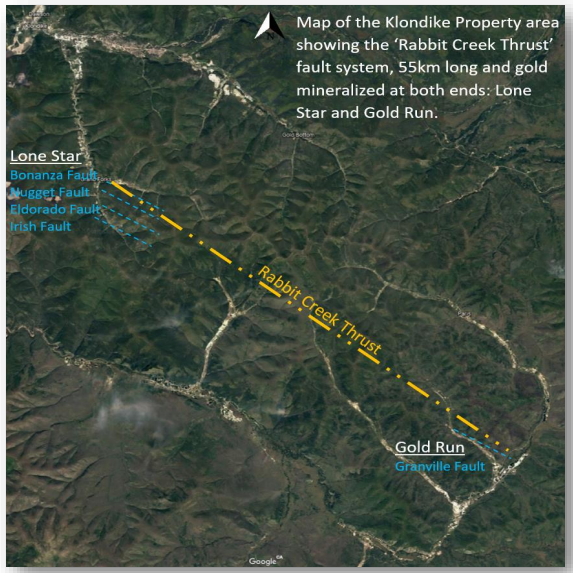

Tallman has identified four faults that control gold mineralization at Lone Star: the Bonanza, Nugget, Eldorado and Irish faults. The gold was forced up through the faults and formed veins or was disseminated. Tallman’s theory is that those faults, in turn, are controlled by the Rabbit Creek Thrust, which he believes could run the entire length of Klondike’s 55-km claims holdings.

“Do we know that these gold-bearing structures, that we’ve proven are at Lone Star, do they extend across the entire 55-kilometre structure?” Tallman says. Determining the answer to that question is the goal of the 2018 exploration program, which will include drilling at Gold Run at the southern end of Klondike’s property.

Klondike Gold has a dominant land position in a district where the mining of gold is already a multi-million-dollar business. A few numbers give a sense of just how large Klondike Gold’s property package is. The company owns 2,780 quartz claims, which make up 553 square kilometres to form a district that is 55 kilometres long. Road access is excellent – an important feature in a territory where planes and helicopters are common but expensive tools of modern gold exploration.

And the infrastructure is about to get better. The $360-million “Roads to Resources” plan announced last year by the Canadian and Yukon governments includes reconstruction of two roads that run through Klondike’s claims. The road connecting Goldcorp’s Coffee to Dawson City also goes through Klondike Gold claims. Goldcorp bought Kaminak Gold and its Coffee deposit — 120 kilometres south of Klondike’s claims — for $520 million in 2016. The takeover was part of a flood of Yukon investments from gold producers including Barrick and Newmont.

Tallman wants to build long-term shareholder value at Klondike Gold, so it’s a play that requires patience. On that front, it helps having deep-pocketed shareholders who take a long-term view of their mining exploration investments. Among them are billionaires Frank Giustra (14%), Eric Sprott (13%) and Francesco Aquilini, whose family owns the Vancouver Canucks hockey team. About 56% of Klondike’s shares are held by the top 20 shareholders.

A series of financings has the company fully funded for both this year and next. Klondike Gold has $6.5 million in the treasury and about $7.4 million worth of warrants.

Since bottoming in the fall of 2016, Klondike shares have been making higher highs and higher lows. Tallman has been buying stock in the open market this year, at prices ranging from 22-24 cents. The purchases take his stake in the company to about 2.7 million shares, or 2.8% of outstanding shares.

Klondike Gold (KG-V, KDKGF-OTC) Price: 0.235 Shares outstanding: 96.8 million (120M f-d) Market cap: $22.8 million

Disclosure: Klondike Gold is one of three Resource Opportunities sponsor companies and James Kwantes, editor and publisher of Resource Opportunities, owns Klondike Gold shares. Readers are advised that this article is solely for information purposes. Readers are encouraged to conduct their own research and due diligence, and/or obtain professional advice. The information is based on sources which the publisher believes to be reliable, but is not guaranteed to be accurate, and does not purport to be a complete statement or summary of the available data.

Copyright: This publication may not be reproduced in whole or in part, in any form, without the express permission of the publisher. Permission is given to extract parts of the report for inclusion or review in other publications only if credit is given, including the name and address of the publisher.

Every junior resource speculator, whether consciously or not, balances risk and reward. The potential for lucrative gains lures investors into this small and notoriously volatile corner of the investment world – the promise of 10-baggers and more. But risk is the admission price for entry. And it comes at a cost, even if the stock is cheap.

Unfortunately, the drill plays that offer the greatest upside potential also carry the most risk. Take too many foolish or reckless risks along the way and you won’t have money left to invest. And today’s high flyer can quickly turn into tomorrow’s pooch. That makes capital preservation a key consideration for junior resource speculators – even though the emphasis is usually on the reward side of the equation. Describing it as the lottery ticket approach to investing is not much of an exaggeration.

Enter project generators, which can allow investors to manage risk while keeping upside exposure in a sector with often binary outcomes. Project generators build value by optioning out properties – and risk – to exploration companies, typically in exchange for cash and shares. The downside is protected by cash, land and proprietary databases, while the shares of optionee companies offer upside. The business method also allows the company to dodge share dilution – a fatal bullet for many juniors.

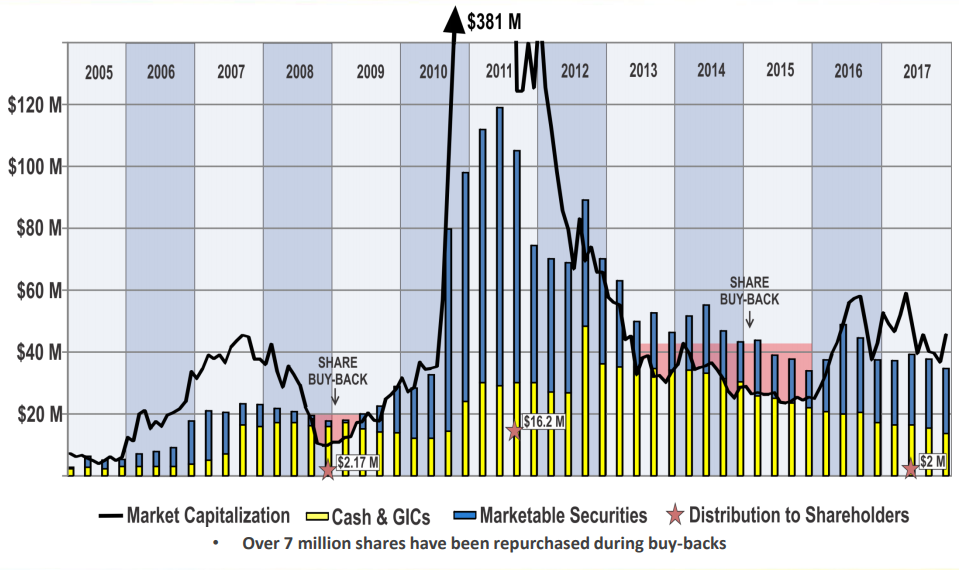

The business model has been successfully demonstrated by Strategic Metals (SMD-V) in the Yukon. Strategic refocused to adopt the generative model in December 2005, starting out with working capital (cash + shares) of 7 cents and the stock at 21 cents. As of Feb. 14, SMD had working capital of 36 cents per share (now 37 cents) and a share price of 48 cents (now 45 cents). There have also been distributions/spinouts of 24 cents a share along the way, including Silver Range Resources (SNG-V) and most recently, Trifecta Gold (TG-V).

That works out to a compound annual growth rate of 7.6% for the stock, assuming dividends are reinvested. The growth in working capital per share – from 7 cents to 36 cents – has been even more impressive. Strategic has a volatile 10-year stock chart, but the spikes offer shareholders higher exit points. During the severe dips, Strategic buys back its own shares. Want explosive upside potential? Strategic has been no slouch, as demonstrated by 2010 and 2011 share price action. High-grade gold discoveries at ATAC’s Rackla property – along with gold’s run to US$1,900 an ounce – lifted Strategic shares above $3 for several months in 2011 (ATAC shares hit $9 that year).

Strategic Metals: working capital vs. market capitalization

With gold approaching 2016 and 2017 highs, Strategic is well-positioned to capitalize. The company’s dominant position in the Yukon positioned it ahead of the herd, allowing it to secure key land positions around all the projects that subsequently saw investment by majors including Barrick, Newmont and Agnico Eagle. In a sector where companies burn through capital, think of Strategic as a business that steadily grows shareholder value with a long-term outlook. As Strategic Metals CEO Doug Eaton puts it, “we don’t have the purity of the exploration plays, but we have leverage to all of them.”

Strategic CEO Doug Eaton checks out samples at Trifecta’s Triple Crown property.

The company’s main edge is the vast geological database of storied Yukon consultancy Archer Cathro, run by Strategic CEO Eaton and his team of geologists and project managers. Strategic’s brain trust has been involved in many of Yukon’s top discoveries and deposits, including Western Copper and Gold’s Casino, Rockhaven’s Klaza and ATAC’s Osiris and Tiger projects. Eaton’s knowledge of the Yukon is encyclopedic and his decades operating in the Northern territory help him snap up neglected and forgotten claims.

Strategic is known as a kind of Yukon-focused investment fund, with extensive shareholdings and a treasury currently at about $13.4 million. But a good argument could be made that the company’s true value is its property portfolio. Strategic has more than 100 fully owned projects available for option, many of them permitted for large-scale drill programs. Among them:

Hopper, a large porphyry-style target where Strategic assayed 0.52% copper over 45.7 metres in a trench. Geochemical surveys outlined strong copper, gold and moly soil anomalies covering a 3,600-metre by 2,500-metre area. Similar age as Western’s Casino deposit 190 km to the north-northwest.

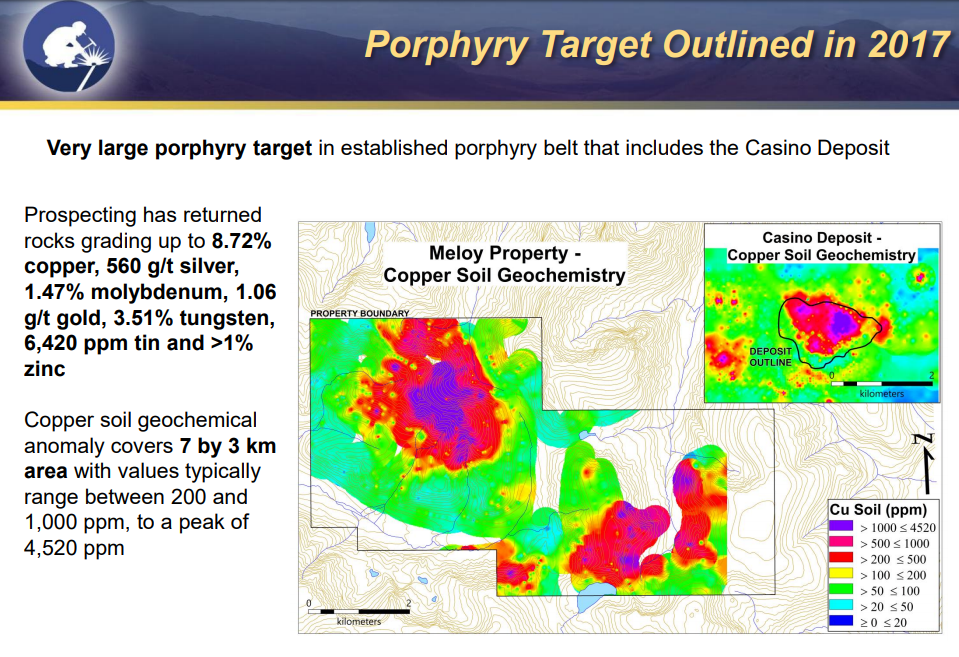

Meloy, another large porphyry target in the belt that includes Casino. Chip samples graded up to 8.7% copper, 560 g/t silver, 1.06 g/t gold, 1.47% moly and 3.51% tungsten.

Strategic owns a 39.7% stake in Rockhaven Resources (RK-V) and has a 7.3% stake in ATAC Resources (ATC-V), among other shareholdings. After a busy drill season, Rockhaven is prepping a resource update and looking at processing changes at Klaza, the Yukon’s highest-grade gold deposit of more than 1 million ounces. Last year Coeur Mining bought a 9.9% stake. ATAC is advancing its Carlin-type gold deposits at the Rackla property and last year attracted a $63.3-million investment from Barrick, which is earning a 70% interest in the Orion project. There are also significant stakes in exploreco Precipitate Gold (PRG-V) and project generator Silver Range Resources, among many others.

The latest Strategic spinout was Trifecta, which is exploring properties in Yukon’s White Gold country and B.C.’s Golden Triangle. Trifecta shares flew out of the gate after listing at 10 cents, briefly trading above 30 cents. But the stock has since settled back down to the 10-cent level after disappointing drill results at the Squid claims at its Trident property. Speaking about Squid, Trifecta CEO Dylan Wallinger had pledged to “prove it or kill it” – the company has subsequently dropped those claims, optioned from Metals Creek Resources.

In addition to developments at portfolio companies Rockhaven and ATAC, there are new potential catalysts in 2018. One of the more interesting new positions will be a 19.9% stake in Territory Metals, a private company expected to IPO on the TSX Venture later this year. Territory purchased six high-grade gold and silver prospects from Strategic, which retains a 2% royalty on all the properties – and a 10% NSR on any small-scale high-grade production.

The six properties, in central Yukon’s Tombstone belt, are Mt. Hinton, Plata, Lance/Lois, News, Naws and Nels. At least a couple of them could provide fireworks. Placer miners have been pulling out multi-ounce rounded gold nuggets – believed to be near source – from Granite Creek, which drains the Mt. Hinton property. Mt. Hinton is located near Alexco’s ground in the Keno Hill district.

Plata, subject to Strategic’s high-grade NSR, also offers intriguing potential. The ore mined at Plata, which is atop a mountain, was very rich. In the 1980s, miners hand-mined and transported it down by helicopter to an air strip at the bottom of the mountain. The ore was then flown to Ross River and trucked all the way down to smelter at Trail, B.C., 2,600 kilometres away. Helicopters, airplanes and truck transport – yet the mining was still profitable.

Strategic has also made a foray into Canadian diamond exploration through a $1-million financing that gave Strategic a 45% stake in diamond exploreco GGL Resources (GGL-V). GGL has property holdings in the Lac de Gras diamond field in the Northwest Territories and a diamond database with more than $30 million worth of exploration data. In November GGL brought in David Kelsch as president and chief operating officer. Kelsch is a Canadian diamond exploration veteran who worked for Rio Tinto and was involved in the discovery of the Diavik diamond mine.

Diamonds have been generating some buzz of late. Dominion Diamond Corp., owner of Ekati and 40% owner of Rio’s Diavik mine, was recently bought for US$1.2 billion and taken private by the Washington Group. Mountain Province Diamonds, meanwhile, purchased Kennady Diamonds – a former spinco – and its Kelvin and Faraday diamond projects in the Northwest Territories for $176 million. GGL Resources has two royalties on Kennady claims, on trend with the Gahcho Kue diamond mine and Kennady’s Kelvin-Faraday corridor.

Strategic Metals (SMD-V) Price: 0.45 Cash: $13.4 million Working capital: $33.3 million (37 cents a share) Shares outstanding: 89.44 million (96.8 fully diluted) Market cap: $40.2 million

Disclosure: Strategic Metals is one of three company sponsors of Resource Opportunities and Resource Opportunities editor James Kwantes owns SMD shares, which makes me biased. Readers are advised that the material contained herein is solely for information purposes. Readers are encouraged to always conduct their own research and due diligence, and/or obtain professional advice. Dollar and $ refer to Canadian dollars, unless stated otherwise.

Site visit: Sabina Gold & Silver (SBB-T)

Oct. 4, 2017

By James Kwantes

Resource Opportunities

Canada’s North is a mysterious and forbidding land. There are stories of European explorers disappearing without a trace and place names such as Deadman’s Island. Native legends from the original occupants – not to mention strangely colourful lights that often dance across the night sky – add to the intrigue. I saw the Northern Lights for the first time during the site visit. The scientific explanation does little to diminish their mystique.

Sabina’s Goose camp, Back River, Nunavut

Flying over the barren lands of Northwest Territories and Nunavut gave me a renewed respect for Chuck Fipke and all the other Northern pioneers who identified mineral deposits there. Between Yellowknife and Sabina Gold & Silver’s Goose camp, the plane travelled over hundreds of kilometres of waterlogged tundra with nary an interruption. Then, rather suddenly, an open-pit diamond mine – a mineralized pin prick in a pin cushion measuring millions of square kilometres. The diamond mine was Diavik; Ekati is nearby.

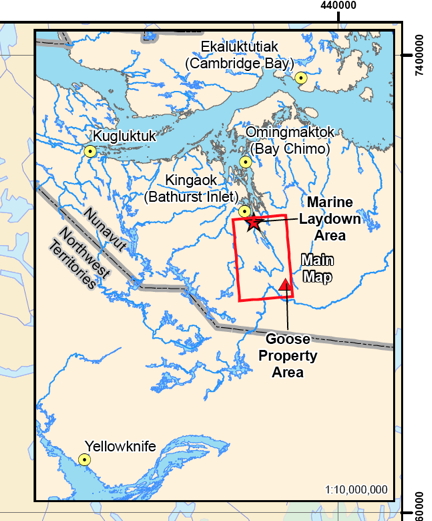

This is about as far from “civilization” as it’s possible to get. For perspective, driving from Billings, Montana to Edmonton, Alberta, a major Canadian northern outpost, takes about 11 hours – roughly akin to driving from Durango, Mexico, to Los Angeles. It takes another 15 hours to drive from Edmonton to Yellowknife — the equivalent of travelling from Los Angeles to Portland. Sabina’s Back River project is a further 520 kilometres beyond Yellowknife, to the northeast.

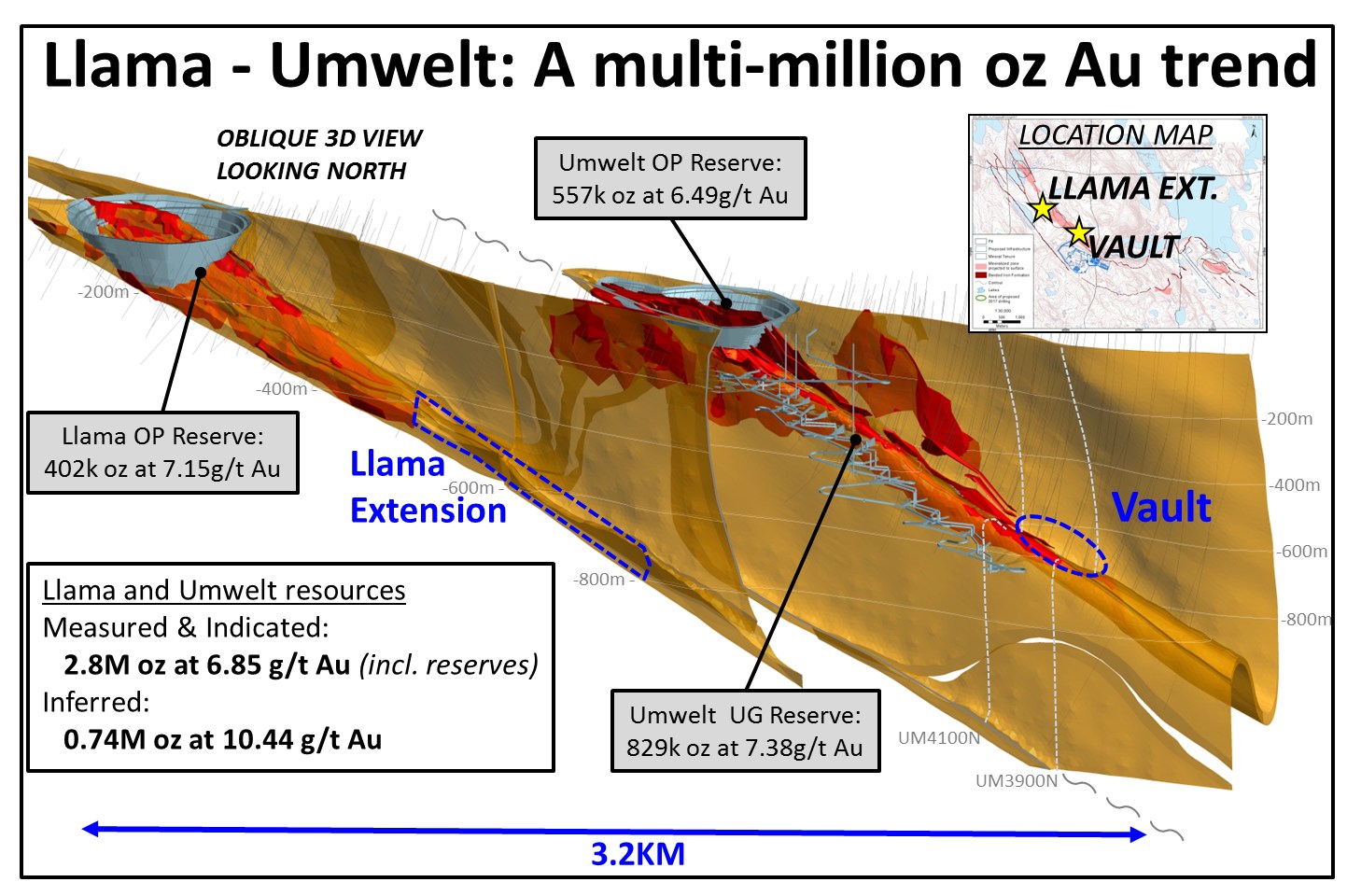

As for Sabina, the main mystery on the company’s vast Back River property may be just how many high-grade ounces are buried under the Arctic tundra. It’s a puzzle this summer’s drill program should go some way to solving. A single early result from the 10,000-metre summer exploration program was promising. The first drill hole, 17GSE516B – released the morning I flew into Yellowknife en route to the site visit – intercepted 9.48 g/t gold over 38.55 metres in a down-plunge extension of the Llama deposit. Not bad for a 460-metre step-out hole. The focus is on adding high-quality ounces — after all, Back River already hosts 7.2 million ounces Au in all categories.

FIRST IMPRESSIONS

Our plane of analysts landed at the Goose camp on a high-quality air strip made from gravel produced on-site. The camp gets its name from adjacent Goose Lake, which serves as the winter landing strip for 737s that come in laden with fuel. The well-run camp felt more like a mining operation than an exploration camp.

Inside, we were briefed on the objectives of the summer drill program and the path forward by CEO Bruce McLeod, VP Exploration Angus Campbell and Exploration Manager Jamex Maxwell. The broad outlines of the mine were established by the initial project 3,000-tonnes-per-day Feasibility Study (3KFS) McLeod commissioned when he took over in February 2015. At US$1,150/oz gold, C0.80 exchange and a 5% discount rate, the FS showed:

– 240,000 oz annually for first 8 years, about 200,000 oz for 12-year life of mine;

– $415 million initial capex, $185M sustaining capex;

– 6.3 g/t Au average head grade, 93% recovery;

– life-of-mine, all-in cash costs of US$763/oz (incl initial & sustaining capex & closure costs)

VP Ex Campbell spoke about uber-high-grade exploration upside (more on that later), while derisking was the major theme for McLeod: “We can’t afford to make mistakes in this part of the world.” Sabina has spent about $5.5 million on basic engineering since the completion of the Feasibility Study, he said, and is now into detailed engineering.

The CEO describes the Back River project as a straightforward mine in a complex environment. From a geotechnical perspective, McLeod says Back River is probably the simplest project he’s been involved with. His assertion was confirmed by a visit to the nearby mill site, the helicopters landing on flat bedrock terrain. One of the benefits of a vast property is the ability to choose exactly where the mill will be. Standing on the flat terrain of scrub and bedrock, with a 360-degree panorama view, it was easy to visualize a mine taking shape.

Author at the site of proposed Goose plant

I found an analogy McLeod used in his recent presentation at the Beaver Creek precious metals summit useful: “To a layperson, a feasibility is a concept, basic engineering is a plan and detailed engineering is a blueprint.” As Sabina constructs the blueprint, the focus is on investing upfront to avoid problems down the road. During the site visit, McLeod talked about his love for technology and some of the high-tech toys at his house, which he said “has lots of gizmos and bells and whistles and shit that breaks down all the time. It won’t happen here.”

It’s not typical CEO bluster: McLeod has already built a mine in Canada’s North. That was Capstone’s Minto copper mine in the Yukon, built by Sherwood Copper and the first hard-rock mine constructed in the territory in a decade. Sherwood was founded and run by McLeod and later bought by Capstone for $244 million. Minto was built on time and under budget – no small feat in Canada’s North.

Sabina CEO Bruce McLeod talks nuts and bolts of a mining operation at Back River.

Recent problems experienced by Nunavut neighbour TMAC Resources (TMR-T) at its recently opened Hope Bay gold mine illustrate the importance of “doing it right the first time.” TMAC recently slashed its annual guidance in half – from 100,000 to 120,000 ounces of gold to 50,000 to 60,000 ounces – due to processing issues and recovery problems. Sabina is paying close attention to metallurgy and a potential processing change from whole ore leach to flotation is one of the optimizations Sabina is studying.

BACK TO THE FUTURE

Some background on Back River: Sabina Silver became Sabina Gold & Silver with its 2009 purchase of the high-grade gold project from Dundee Precious Metals (DPM-T). Prior to that, the flagship was the silver-rich Hackett River VMS deposit 45 kilometres to the west, which Sabina sold to Xstrata (now Glencore) in 2011 for $50 million cash and a significant silver royalty. That transaction put Sabina into the rare category of well-funded junior, where it remains. More on the silver royalty later.

Sabina has since added about 5 million ounces, bringing the Back River resource to 7.2 million ounces in all categories. Most of the added ounces were drilled in the first two years, followed by a lull in drilling during the 2011-16 bear market. The most recent drill program has taken the number of metres drilled above 500,000.

The scale of the core-cutting facility at Goose is an indication of the size of previous programs. It can comfortably handle 85,000 metres in a single season, so is not stretched at 10,000 metres, McLeod noted. It may seem like a minor detail, but is another box ticked for any major that buys the district-scale project (Goldcorp, for example, is carrying out an aggressive exploration drill program at Coffee).

The Back River project is a banded iron formation project that consists of 10 high-grade gold deposits on Sabina’s 53,000-hectare properties. It’s an 80-kilometre district. Llama is one of four deposits at the main Goose project area, the focus of the 3KFS that McLeod commissioned. (An earlier FS modelled a 6,000tpd operation producing 350,000 oz over a 10-year mine life.) Three of the four Goose deposits are part of the 3KFS: Goose main pit, Umwelt open pit and underground and the Llama open pit. The Llama underground, including hole 17GSE516B, is not.

ECONOMICS OF EXPLORATION

One of the objectives of Sabina’s drilling is to determine if there are enough high-grade ounces underground to define a “treasure box” that could be mined up front. If the company is successful, that would involve shifting sustaining capex into the front end of the mine plan. But it could significantly improve already strong project economics, especially at the front end of the mine life. An increase of just 500 tonnes per day – to 3,500tpd – could vault Sabina into 300,000 oz/year territory.

Angus Campbell, Sabina’s VP Exploration, shed some light on how rich some of the exploration potential is on Sabina’s ground. Being the guy in charge of running exploration programs in a gold-rich 80-kilometre belt must have a kid-in-a-candy-store feel to it. But with McLeod in charge of the candy allocation, Campbell’s targets must be chosen wisely and justified. Despite 500 kilometres of drilling, there remain multiple opportunities for resource expansion, both at existing deposits and at deposits not included in either Feasibility Study.

Consider Sabina’s George deposits, about 50 kilometres away from Goose. George hosts about 2.1 million gold ounces included in the 6KFS but NOT in the 3KFS. Drilling there in the 1980s, outside the resource envelope, also hit several wide, shallow intersections of 6 and 7 g/t Au, McLeod said – rich ore by any standard. Sabina geologists were puzzled why these near-surface intercepts were not followed up at the time.

The answer, from people directly involved in the drill programs: the predecessor company was looking for higher Lupin-like grades of 9 and 10 g/t material. The nearby Lupin mine produced about 3.35 million ounces of gold between 1982 and 2004 at an average head grade of 9.27 g/t.

Under the 6,000tpd plan, George ore was slated to be trucked to the mill at Goose. But McLeod believes George is destined to become a second standalone mine once Goose is put into production. It’s a strategy both Agnico Eagle (Amaruq) and TMAC Resources (Boston) are following with their multi-deposit Nunavut gold districts.

EXPLORING A VAULT

The greatest upside potential, however, is probably where Sabina is drilling now – at the Llama extension and the Umwelt Vault zone. Particularly the latter. Vault assays are outstanding from the summer drill program, which included about 4,000 metres of Vault drilling. A spring hole there hinted at the richness, returning 16.86 g/t gold over 13.5 metres, including 27.11 g/t over 7.95 metres.

Oblique longitudinal section of the Llama/Umwelt trend target areas.

The Vault targeting is follow-up from rich 2011-12 intercepts, including 17 metres of 49.24 g/t Au. For perspective, that grade is roughly equal to GT Gold’s (GTT-V) recent intercept that helped send that Golden Triangle-focused play to a $200-million market cap briefly (Sabina’s market cap is $515 million). Except Sabina’s 2012 hole was 17 metres, compared to 6.95 metres for GTT. I asked VP Ex Angus Campbell why the rich hits weren’t followed up on at the time – he said the focus then was on building open-pit ounces.

On the infrastructure and development front, Sabina plans to truck supplies to the mine via a 157-km winter road built every year at a cost of $8 million. The CEO described it as a “fairly simple” road, logistically. Sabina will have about 45 days to truck supplies from the marine laydown area, in southern Bathurst Inlet, to the Goose camp.

Sabina is not banking on it, but a Northern road plan that has been decades in the making could also intervene to lower costs for the project. That’s the Grays Bay port and road initiative, a plan for an all-season 230-km road from a deep-water Arctic port that connects to the Yellowknife winter road. With the buy-in of the Kitikmeot Inuit Association, which also strongly supports Back River, this iteration of the plan looks closer to reality than it has for some time. The road would be closer to the George deposit than Goose, but could result in significant savings.

THE PATH FORWARD

Resource Opportunities initiated coverage on Sabina Gold & Silver on May 18, 2015, during the bear market. The catalyst for coverage was McLeod’s hiring. When I met him and Sabina’s VP Communications Nicole Hoeller in a Vancouver coffee shop, McLeod gave me a taste of his tenacity: “My philosophy is like the Italian rule of driving: you rip the rear-view mirror off, put your foot on the gas and it doesn’t really matter what’s behind you but you’re moving forward … You’re not going to let your foot off the gas.” The line implies recklessness, but it’s more about a single-minded focus on advancing projects.

McLeod could not have foreseen the dark days of summer 2016, but the philosophy served him well during that period. That’s when the Nunavut Impact Review Board (NIRB) recommended to the federal government the rejection of the Back River project as currently constituted, despite widespread Inuit and community support. The reasons given were concern over caribou and climate change implications. Ottawa flipped the tables, rejecting the NIRB’s conclusions and ordering the regulatory agency to re-examine its findings. That resulted in a positive recommendation. A final ruling from the federal government is expected before year-end.

The number of high-quality gold discoveries in recent years has dropped along with the exploration budgets of the majors. Ore grades have steadily fallen and the miners are more reliant than ever on junior exploration companies to fill the supply gap. There are precious few district-scale, high-grade gold projects in safe jurisdictions. Sabina’s Back River fits the bill and has no fatal flaws. I expect Sabina to be acquired by a large gold mining company, at prices well above the current levels. In a rising gold price environment – not a given, a bidding war could well be the outcome.

CONCLUSIONS

I have described Sabina previously in the newsletter as a kind of triple leverage play, and it still holds true. The shares were at bear market levels of 39 cents when I initiated coverage, and Sabina had 194 million shares outstanding. Importantly, the share count has risen only 30 million since then as the stock has increased sixfold.

That’s in the rear-view mirror, of course, and the key question is what kind of upside exists from current levels. Gold is showing weakness again, following an increase through US$1,300/oz and rapid rise to $1,350. But I expect the precious metal to resume its rise in an easy-money world, and Sabina’s 7.2 million ounces make the company’s shares an ideal vehicle for exposure to gold. I have added to my position at levels above the current share price. The following factors give Sabina multibagger potential from these levels, and tremendous leverage:

Exploration – Drill plays have been getting much of the love in recent months. GT Gold Corp and other plays focused on British Columbia’s Golden Triangle plays have been leading the charge, but there have been others. The junior market’s enthusiasm for drill plays and ambivalence towards development plays reminds me of the Benjamin Graham quote: “In the short run, the market is a voting machine but in the long run it is a weighing machine.” Sabina’s recent drill results compare favourably with many drill plays that have added tens of millions of dollars of market cap on favourable assays. In Sabina’s case, the assays are overlain on a very high-grade, FS-stage gold project and potentially have a direct favourable impact on project economics. Votes come and go but the weight remains.

Takeover premium. Recent takeover premiums in the gold space have been at healthy premiums (see below). In Sabina’s case, the strength of the project means the premium should at least match the highest-ranking, Integra at about 50%. That offer came from a major (Eldorado Gold) that already owned about 13% of Integra shares. Sabina has no such partner, one of the reasons a bidding war is quite possible. Dundee Precious Metals and Sun Valley Gold are the largest shareholders, each with just above 10%. Here are the takeover premiums a few of the more recent takeovers. The premium to the last close is first, followed by the premium to the 20-day volume-weighted average share price:

3. Silver royalty: Sabina retained a valuable royalty when it sold the prior flagship project, the Hackett River polymetallic deposit, to Xstrata (now Glencore). It’s a 22.5% royalty on the first 190 million ounces of silver produced, and 12.5% on the remainder. Hackett River is one of the world’s largest undeveloped VMS deposits and the main price is zinc. Zinc has soared from below US70 cents/lb in January 2016 to about $1.40 today. The royalty was previously assigned a value of $300 million by analysts, and McLeod contends it would trade at a valuation of $300-$400 million in the portfolio of a larger royalty company such as Wheaton Precious Metals or Royal Gold. The silver royalty gets little to no value in Sabina’s portfolio.

Suitors? It’s a long list. Goldcorp has telegraphed its intention to only acquire district-scale projects, and Back River fits the bill. The project is superior on almost every level – grade, size, scalability – to Kaminak’s Coffee project and Goldcorp spent $520 million to purchase that operation. This is pure speculation, but I bet B2Gold CEO Clive Johnson would also love to open a high-grade gold mine in Canada to go with operations in more exciting jurisdictions that include Mali, the Philippines and Burkina Faso.

Management is the single most important ingredient in the junior mining sector, and Sabina’s is impressive. When he took over as CEO, McLeod refocused the company, trimming some fat and beefing up insider skin in the game. Under his stewardship, Sabina has smartly increased the quality of the gold ounces while controlling the share structure. I was impressed during the site visit by both VP Ex Angus Campbell and Exploration Manager James Maxwell.

Finally, a small detail. Sometimes, they tell a tale. There was no swag on the site visit – company shirts, ball caps, pens, etc – and clearly cost considerations were front and centre for Sabina. I’ve seen lots of swag from plenty of lesser projects in my travels. As a shareholder, seeing that kind of focus on the lesser details reassured me that Sabina will pay close attention on the big details, too – such as a fair takeout price.

Sabina Gold & Silver (SBB-T) Price: $2.30 Shares outstanding: 224 million (243M f-d) Treasury: $36.6 million (as of June 30, not including financing proceeds) Market cap: $515.2 million

Disclosure: I own shares of Sabina Gold & Silver and the company paid for costs associated with the site visit. Readers are advised that the material contained herein is solely for information purposes. Readers are encouraged to conduct their own research and due diligence, and/or obtain professional advice. Nothing contained herein constitutes a representation by the publisher, nor a solicitation for the purchase or sale of securities. The information contained herein is based on sources which the publisher believes to be reliable, but is not guaranteed to be accurate, and does not purport to be a complete statement or summary of the available data. Any opinions expressed are subject to change without notice. The author and their associates are not responsible for errors or omissions. They may from time to time have a position in the securities of the companies mentioned herein, and may change their positions without notice. (Any positions will be disclosed explicitly.)

IDM Mining is a Resource Opportunities sponsor company.

In the summer of 2016 I visited IDM Mining’s Red Mountain high-grade gold project in northwestern British Columbia for the first time, and most of the underground workings were still flooded with water. The conditions were a testament to the project’s mothballed status before IDM took over. To the weather, as well: the mountains outside of Stewart get plenty of precipitation in the form of both rain and snow. Some fell during that mid-summer visit.

When I returned recently, most of the water in the two kilometres of underground workings had been pumped out. Our group of analysts and investment bankers was able to hike deep inside the mountain. We crossed the portal and CEO Rob McLeod walked us through a damp, dark world, past several crosscuts accessing mineralized zones as well as sites where the underground drill was turning.

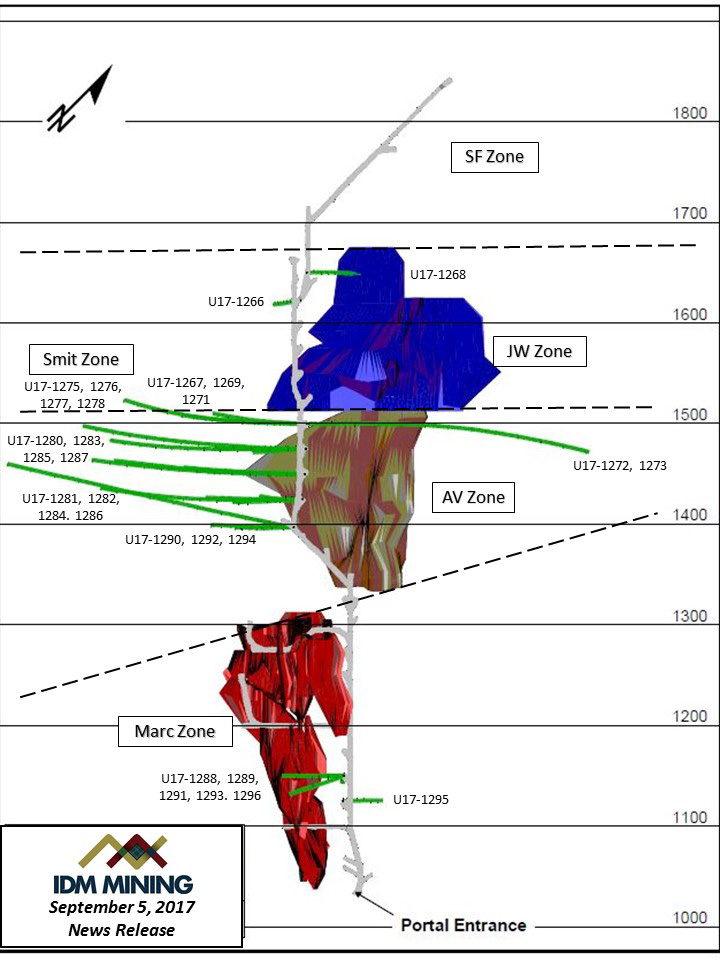

The gold grades have to be rich to make a mine economic in such an environment, and Red Mountain ore is. IDM’s latest intercepts, announced Sept. 5, are the highest-grade ever recorded at Red Mountain: 4.9 metres of 149.2 g/t gold and 59 g/t silver in the Marc Zone, the first mineralized area to be mined. The hit included 0.5 metres of 1,400 g/t Au and 437 g/t Ag. Average grades of reserves at Red Mountain are 7.53 g/t Au and 21.86 g/t Ag – multiples of global grades being mined.

Underground drilling

Majors including Lac Minerals and Royal Oak Mines spent several million dollars blasting out the portal and underground decline before abandoning the project, which IDM CEO Rob McLeod had worked on as a junior geologist. IDM optioned the 17,125-hectare project in 2014 and has systematically advanced it to the permitting stage. A recently published Feasibility Study shows an after-tax NPV of $104 million with an IRR of 32% and a 1.9-year payback, at a 5% discount. That’s based on US$1,250/oz gold and a 76-cent Canadian dollar. Average life-of-mine head grades are 7.53 g/t Au and 21.86 g/t Ag. By comparison, the average gold grade of producing mines, globally, is about 1 g/t Au.

Red Mountain is located in a beautiful corner of the world populated by snowy mountain peaks, glaciers and scenic vistas. We hiked to the top of a ridge as CEO McLeod gave us a tour that was equal parts geology and history. The bird’s-eye view included Bromley Humps, the area that will host the mill and the tailings area (we later visited by helicopter).

IDM Mining CEO Rob McLeod points toward the mill/tailings facility location in the Bitter Creek Valley.

The Golden Triangle’s history of high-grade gold mining points to its potential. Pretium’s Brucejack is just the latest in a region with a long list of past producing high-grade mines, including Snip, Eskay Creek, Premier and Granduc. And IDM’s development is part of a Golden Triangle revival that is driving some incredible share price gains among area drill plays. The most notable is GT Gold Corp., whose shares started 2017 at 25 cents and have rocketed above $2.50 on drill results. The stellar initial intercepts included 6.95 metres grading 51.53 g/t gold and 117.38 g/t silver. The stock surge has vaulted GT Gold to a market capitalization of almost $200 million. That compares to about $50 million for IDM, whose Red Mountain is an FS-stage advanced development project with a defined deposit and lots of upside.

Proven and probable reserves at Red Mountain contain 1.953 million tonnes at an average grade of 7.53 g/t Au, for 473,000 gold ounces, and 21.86 g/t Ag, for 1.373 million silver ounces. Most of the ore is found in three mineralized zones: the Marc, AV and JW Zones. Underground step-out drill results released by IDM this summer hint at the upside potential at Red Mountain. Intercepts have included:

4.9 metres of 149.2 g/t Au & 59.9 g/t Ag, incl. 1,400 g/t over 0.5m (U17-1289, Marc Zone)

8 metres of 12.28 g/t Au & 27.07 g/t Ag (U17-1274, SF Zone step-out)

14 metres of 10.65 g/t Au & 17.37 g/t Ag (U17-1262, JW Zone step-out)

8.6 metres of 12.33 g/t Au & 70.9 g/t Ag (U17-1245, JW Zone step-out).

Other high-grade Canadian gold plays are being picked off by majors, one by one. Recent projects that have been purchased include Lake Shore Gold ($945 million by Tahoe), Kaminak ($520 million by Goldcorp) and Integra ($590 million by Eldorado). The latest to be snapped up was Richmont Mines, a high-grade underground producer recently acquired by Alamos Gold for $933 million. Richmont produces gold at two underground mines in Ontario and Quebec.

In USD terms, the price of gold has increased about 15% this year, from $1,150 to the current $1,325. Yet IDM shares have remained at the 14-cent range, after hitting 21 cents about a year ago. Here are five reasons IDM shares are worth a closer look at these levels:

1. GRADE

The global gold mining industry is facing a supply crunch. Demand remains strong, driven primarily by the Asian appetite, ETF inflows and central bank buying. But on the supply side, gold mining companies are struggling to keep pace. It’s primarily due to a lack of new discoveries, a trend that is forcing miners to process lower-grade ore as they deplete existing ore bodies. The average grade at producing gold mines, globally, is about 1 g/t Au. It’s a worrying industry trend since grade remains king, as well as being a key determinant of the profitability of gold mining companies. That puts a target on IDM Mining’s Red Mountain, which has gold grades multiples of the global average. Cash costs net of silver credits for the Red Mountain project would be US$492/oz, according to IDM’s recent Feasibility Study.

2. INFRASTRUCTURE

Smart management teams purchase unloved, unwanted assets for pennies on the dollar during bear markets, then turn them into viable economic projects in time for the commodity upcycle. That’s the playbook for IDM and the timing looks good, especially with gold’s push above $1,300/oz. IDM leveraged millions of dollars of prior development, including almost 2,000 metres of underground tunnels. The infrastructure advantage extends to road access from Stewart, as well as plentiful and cheap power. British Columbia has some of the least-expensive industrial power rates of any jurisdiction in the world.

3. TEAM

Stewart is Rob McLeod’s hometown and he has deep family roots there, which makes construction of a mine at Red Mountain personal. The town of Stewart used to be a thriving mining hub but is heavily exposed to the cyclicality of the sector. For example, Stewart’s 1910 population of 10,000 dropped as low as 17 people less than a decade later, during the First World War years. Rob’s father Ian McLeod and his uncle Don (after whom IDM is named) prospected mountains in the region for gold – including the property that now hosts Pretium’s high-grade Brucejack mine. Stewart boomed again with the opening of the Premier mine, which operated from the 1920s to 1952 and was North America’s largest gold mine.

How deep are the CEO’s ties to Stewart? Rob’s father was born in Stewart in 1927 and served as mayor for 15 years. He also owned the King Edward Hotel in Stewart from 1952 to 2001. IDM’s Executive Chairman is Mike McPhie, a mining veteran who was CEO of Curis Resources (bought by Taseko Mines) and a director of Silver Quest Resources (bought by New Gold). Another third-generation miner, engineer Ryan Weymark, joined IDM Mining in the spring. His father and grandfather were also mining engineers and spent their careers at Teck Cominco.

4. RESOURCE UPSIDE

IDM’s high-grade stepout hits at Red Mountain mean the 5.4-year mine life outlined by the Feasibility Study is likely to be extended, perhaps considerably. Infrastructure costs for a mine would be fixed, so finding additional ounces is highly accretive to mine economics. And the upside goes beyond defining additional ounces at Red Mountain. Glacial melt has uncovered areas of mineralization that have never been drilled or explored, such as Lost Valley. A resource update is expected in the first quarter of 2018.

Lost Valley gold mineralization

5. STRIKEPOINT GOLD STAKE

A deal IDM announced in late 2016 has given the company a call option on a promising portfolio in the Yukon, one of the world’s hottest exploration jurisdictions. The company sold its Yukon projects (formerly owned by Ryan Gold) to Strikepoint Gold (SKP-V) for $4 million, most of it in StrikePoint shares. As a result IDM holds 18% of StrikePoint’s outstanding shares, joining other major shareholder Eric Sprott, who owns a 12% stake. StrikePoint’s VP Exploration is Yukon veteran Andy Randall, who was chief geologist for Ryan Gold when that Shawn Ryan vehicle spent $25 million to advance the Yukon projects. StrikePoint is spending $2.5 million this year to explore three properties: Mahtin, Pluto and Golden-Oly. The fledgling company, helmed by Shawn Khunkhun, has about $8 million in the treasury and is fully funded through 2018. IDM’s stake is worth about $2.9 million at StrikePoint’s current share price.

Disclosure: IDM Mining is a Resource Opportunities sponsor and the author is long IDM Mining shares, which makes him biased. This article is for informational purposes only. All investors are responsible for their own trades and need to do their own research and due diligence.

Columbus Gold advances Montagne d’Or towards bankable feasibility study

Fall resource estimate planned at Eastside gold project in Nevada

By James Kwantes

Resource Opportunities

As befits its location about 500 kilometres north of the equator, French Guiana is hot and humid, with average temperatures of 25-30 Celsius year-round. The namesake Cayenne pepper, named for the capital city, spices up cuisine and hints at the Creole roots of the territory, a region of France.

But it’s the heat being generated by a rising gold price that could help revitalize the economy of French Guiana. It’s a prosperous corner of South America, but GDP remains heavily reliant on the Guiana Space Centre. Selected in 1964 to be France’s space centre, the facility expanded to become Europe’s Spaceport in 1975 and is used by other countries launching satellites into space, including Russia.

The Guiana Space Centre. Photo: www.satellitetoday.com

Once you step off the space centre, however, incomes fall back to earth. French Guiana is heavily reliant on mainland France for subsidies, trade and goods. Traditionally, the region’s main industries have been fishing, logging and small-scale gold mining.

It’s gold that Vancouver entrepreneur Robert Giustra is eyeing. Specifically, the mountain of gold — Montagne d’Or — contained in the deposit that his Columbus Gold is advancing in the jungle 180 kilometres west of the capital city Cayenne. Gold miner Nordgold is earning in to a 50.01% interest in the project by spending at least US$30-million on exploration and delivering a bankable feasibility study by March 2017. In January Columbus sold an additional 5% interest in the project to Nordgold, so their interest would be 55.01% upon completion of the earn-in.

A mine like the one Columbus Gold is proposing would employ about 1,000 people during construction, 800 full-time during operations, and produce an average 270,000 ounces a year. With average mined grades of about 2 g/t in the first 10 years, it would be among the highest grade open-pit gold mines in the Americas.

A WIN FOR FRENCH GOVERNMENT, CGT SHAREHOLDERS

For French Guiana, a large-scale commercial mine would be a game changer, diversifying the economy and boosting the French government’s tax take. It could even help the long-running battle against illegal gold miners in French Guiana. The mostly Brazilian “garimpeiros” use mercury to process the gold and cut a toxic path through the jungle, devastating the environment. The miners then vacate the country with their heavy equipment and the gold, leaving France to clean up the mess.

It’s a problem French authorities have grappled with for a long time, through regular sweeps and arrests. But the illegal miners have the edge through strength of numbers and an intimate knowledge of the jungle. All too often, crackdowns resemble a law enforcement version of arcade game Whac-A-Mole.

The path towards a gold mine at Montagne d’Or could well be a road to riches for shareholders of Columbus Gold, which is also drilling the Eastside gold exploration project in Nevada. Columbus has aggressively developed Montagne d’Or since picking up the project in 2011 when it had a 1.9-million-ounce resource (Inferred). Columbus has delineated 3.9 million ounces in the Indicated category and another 1.1 million ounces Inferred at grades well above global averages.

Last year the company published a preliminary economic assessment for Montagne d’Or showing positive economics at a gold price of US$1,200/oz:

– After-tax NPV of US$324 million (8% discount rate)

– After-tax IRR of 23%

– Initial capex of US$366 million, including US$44 million contingency

– All-in sustaining costs of US$711/oz

– Average annual production of 273,000 ounces at average grades of 2 g/t in Years 1-10

Gold’s rise of more than 27% in 2016 should further improve economics in the Feasibility Study, and it’s not the only factor that will help. The PEA envisioned diesel power being generated on-site at a cost of about US.20/kWh. Columbus is now looking at connecting to the French Guiana grid, which would lower costs to .11-.12/kWh. It’s a substantial savings, since power is one of the mine’s largest operating costs.

In addition to improving economics at the flagship project, gold’s ascent to US$1,350 an ounce has increased the interest level in Columbus Gold shares. The company uplisted from the TSX Venture to the Toronto Stock Exchange on January 26, an accomplishment achieved by only one other company in the previous two years, and shares recently hit 93 cents, a 52-week high.

Robert Giustra, Columbus Gold Chairman & CEO

Sentiment has shifted dramatically from the bear market that took gold down from US$1,900 an ounce to below $1,100/oz, notes Giustra, Columbus’s Chairman and CEO. The resulting flight of capital over the past four years led to liquidity drying up, wreaking havoc on the ability of junior mining firms to raise money and depressing share prices — even for companies with fundamental value. In order to initiate a position, funds would have to sell an existing holding, and there was nobody to sell to. It had the effect of putting the brakes on shares of all mining sector companies, including Columbus Gold. “People would love the story, but couldn’t buy the stock,” Giustra commented.

Capital and interest has returned to the sector, he says, and Columbus Gold shares should continue to benefit. The company has about $4 million in the treasury and two major catalysts on the horizon:

– The bankable feasibility study at Montagne d’Or;

– A planned maiden resource estimate at Eastside, the Nevada project.

EXPLORATION UPSIDE AT MONTAGNE D’OR

Exploration upside around the defined deposit has the potential of turning Montagne d’Or into something even bigger. The aggressive three-year timeline that Nordgold agreed to when it took on the project in March 2014 means little exploration work has been done. That’s despite indications the mineralization at Montagne d’Or remains open along strike to both the east and west, in parallel zones and untested nearby surface anomalies, as well as at depth.

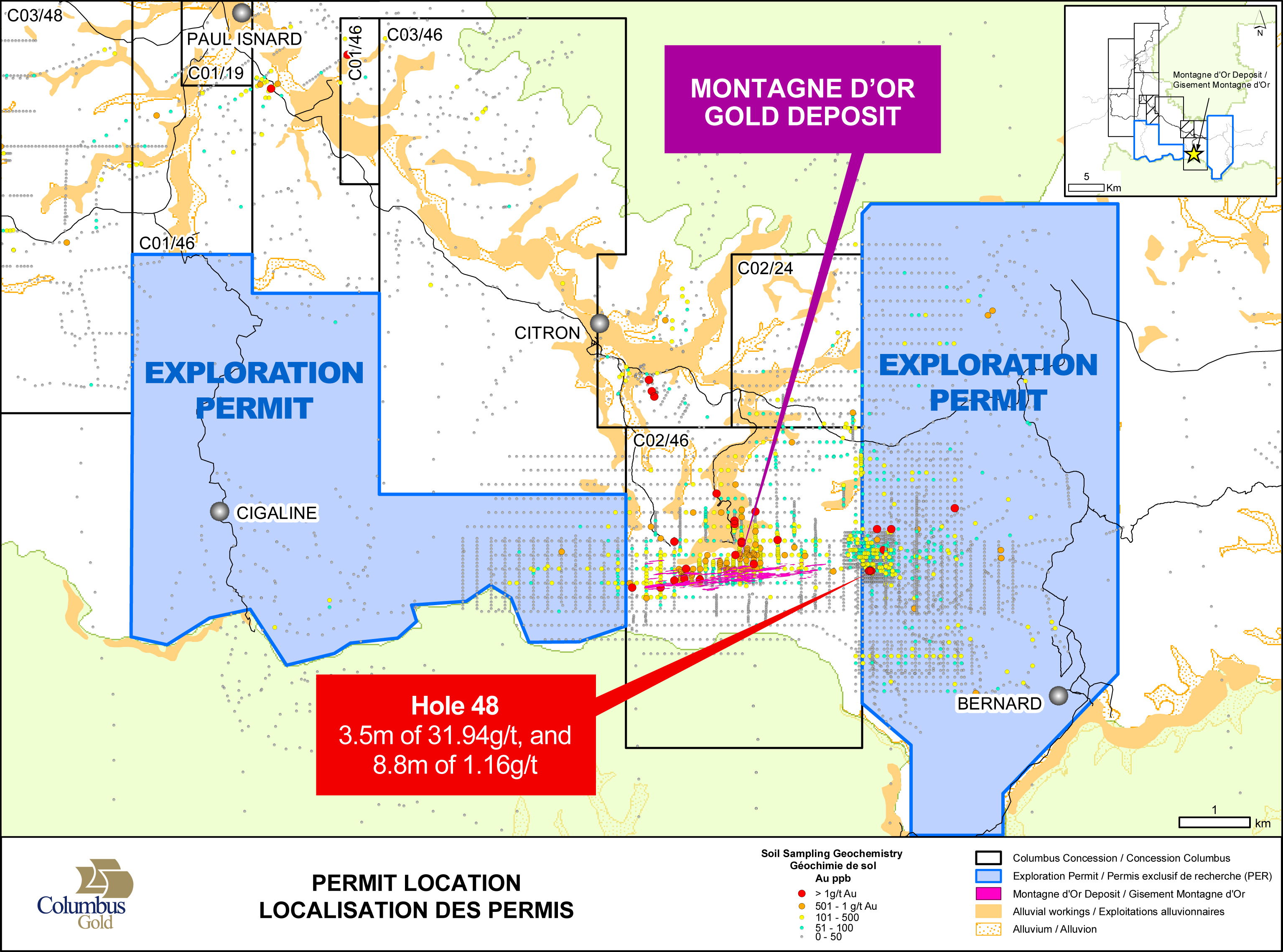

The most recent exploration permits, granted in July by the French Minister of Economy, cover gold-soil anomalies two kilometres to the west and 2.7 kilometres to the east of the deposit. Only two holes have ever been drilled in these areas. One of them, punched in 750 metres east of the deposit, intercepted 31.94 g/t gold over 3.5 metres. Montagne d’Or is also open at depth below the 250 metres modelled by the pit.

Exploration permits on strike of the east and west extensions of Montagne d’Or

The Phase 1 exploration program kicks off this month with prospecting and soil sampling west of Montagne d’Or. For the second phase, Columbus may fly IP (induced polarization) to enhance drill targets. In the 1990s, such geophysical surveying helped trace the gold-sulphide mineralized horizons at Montagne d’Or.

The French geological survey identified the initial gold anomaly that defines Montagne d’Or in the 1990s. But the agency was subsequently privatized and began selling assets including Montagne d’Or, which saw very limited drilling in the late 1990s. Columbus Gold built the resource with drilling campaigns, but the aggressive three-year path to a bankable FS agreed to by Nordgold in March 2014 effectively put a cap on exploration drilling.

As a result, the highly prospective properties that surround Montagne d’Or are virtually virgin territory.

“French Guiana is extremely under-explored, particularly compared to its geological twin in the West African Birimian Shield,” Giustra explains. “That gold region has seen over a century of exploration.”

Geological continuity between Guiana Shield and Birimian Shield

Having a deep-pocketed major pay the bills on flagship development project Montagne d’Or also helped Columbus Gold weather the bear market storms. Nordgold is the world’s 15th largest gold miner and operates 9 mines in 4 countries. In 2015, the Russia-based producer mined about 950,000 ounces at all-in sustaining costs of US$793 an ounce, making it one of the world’s lowest-cost producers. At 270,000 ounces a year, Montagne d’Or would be the largest mine Nordgold has an interest in.

Nordgold also has a reputation as an efficient and smart operator. The Russia-based miner built its newest mine, the 200,000-oz/yr Bissa gold mine in Burkina Faso, in just 15 months, Giustra points out. The company is also familiar with the geological neighbourhood because it operates three mines in the West African Birimian Shield — two in Burkina Faso, one in Guinea.

Nordgold was founded in 2007 as a division of Russian steel giant Severstal and went public on the London Stock Exchange in January 2012. The company is among the world’s fastest-growing gold miners, a feat accomplished mostly through acquisitions.

“People have said to me ‘Watch out for the Russians,’ ” Giustra says, “but they’ve been great partners. We come to agreements on a handshake and they follow through.”

DRILLING SUCCESS AT EASTSIDE IN NEVADA

Columbus Gold also has a growing Nevada exploration project to go with its Montagne d’Or development project in French Guiana. And the company’s foundation for growth lies under the desert sand at its Eastside project.

Nevada’s gold endowment is well-documented. The state produces about three-quarters of U.S. gold production and more than 6% of the world’s gold. Gold mines in the “Silver State” have been company makers for the world’s largest gold producers, including Barrick Gold and Newmont Mining — not to mention royalty giant Franco-Nevada.

Much of that production has come out of the Carlin Trend, one of the world’s richest gold endowments and home to Barrick and Newmont’s most prolific mines. The Carlin was discovered by legendary geologist John Livermore, who sparked a modern-day gold rush when he discovered a new kind of “invisible gold” mineralization in the early 1960s while working for Newmont. He founded Cordex Exploration in 1970 and went on to discover several Nevada gold mines. Livermore died in 2013.

Geologist Andy Wallace, Livermore’s longtime business partner, is now principal of Cordex Exploration as well as president of Columbus Gold Nevada. Wallace joined Cordex in 1974 at the height of the Nevada gold rush and became Cordex’s Manager of Exploration in 1985. He also has a few mine finds under his belt — under his leadership, Cordex discovered the 5-million-ounce Marigold deposit and the 12-million-ounce Stonehouse/Lone Tree deposits. Silver Standard purchased Marigold from Goldcorp and Barrick in 2014 and Lone Tree is still being mined by Newmont.

Columbus Gold Nevada President Andy Wallace is credited with discovering Marigold, now a Silver Standard mine.

Nevada is elephant country for gold. In Cordex, Columbus has an elephant hunter on its team. Columbus has an exclusive exploration arrangement with Cordex, giving the company one of the largest databases in Nevada. Cordex also runs Columbus’s exploration programs in Nevada.

Exploration is now focused on the Eastside project, composed of 725 mining claims making up 57.7 square kilometres about 32 kilometres west of Tonopah, Nevada. The nearby Round Mountain gold mine, which has produced more than 12 million ounces and is now 100% owned by Kinross, is about 32 km away. It’s the world’s largest heap-leach operation.

Columbus recently wrapped up its 2016 drill program at Eastside, completing 17,500 metres of drilling– 12,663 metres of reverse circulation and 4,837 metres of diamond drilling. The company has now drilled more than 37,000 metres at Eastside, mostly confined to a one-square-km parcel dubbed the “Original Target.” Columbus is aiming to complete a maiden resource estimate this fall. Results year-to-date have been positive, with recent intercepts of 97.5 metres of 0.68 g/t gold and 13 metres of 1.12 g/t. Previous hits included 35.1 metres of 4.1 g/t and 152.4 metres of 0.71 g/t.

Gold and silver mineralization at the Original Target occurs in two broad, northerly trending zones called the East Zone and West Zone. The zones coincide with rhyolite flow dome complexes that host the bulk of the mineralization. Drilling to date has determined that strike extends at least 450 metres on the East Zone and 850 metres on the West Zone. Both zones are open at depth and to the south, and the West Zone is open to the north as well.

Initial metallurgical tests determined that gold at Eastside is highly amenable to processing using cyanide. Columbus is now doing further metallurgical tests on samples of varying grades and ore types to evaluate potential heap leaching and whether crushing will be required and if so, the optimum crush size.

Eastside is located in an infrastructure sweet spot. It’s adjacent to Highway US95, the main road route between Las Vegas and Reno, and is connected by a county-maintained gravel road. A major transmission line runs through the Eastside property and there is available water from shallow aquifers in the area, Giustra says. Year-round drilling is possible at the property.

Infrastructure is excellent at Eastside, located about 32 km west of Tonopah, Nevada

If Columbus Gold can connect the dots and mineralization at Eastside, the Nevada gold property could become an impressive flagship project. In Cordex, Eastside has an experienced minefinding partner. The project’s good metallurgy, superior road infrastructure, power and water access lower the threshold to develop a mine in America’s most important gold-producing state.

Price: 0.76 Shares outstanding: 142.9 million Market capitalization: $108.6 million Treasury: $4 million

Disclosure: The author owns shares of Columbus Gold and the company is one of a small number of Resource Opportunities sponsors, who help support the subscriber-funded newsletter. The work included in this article is based on SEDAR filings, current events, interviews, and corporate press releases. It may contain errors, and you shouldn’t make any investment decision based solely on what you read here. This publication contains forward-looking statements, including but not limited to comments regarding predictions and projections. Forward-looking statements address future events and conditions and therefore involve inherent risks and uncertainties. Actual results may differ materially from those currently anticipated in such statements. This publication is provided for informational and entertainment purposes only and is not a recommendation to buy or sell any security. Always thoroughly do your own due diligence and talk to a licensed investment adviser prior to making any investment decisions. Junior resource companies can easily lose 100% of their value, so read company profiles on www.SEDAR.com for important risk disclosures. It’s your money and your responsibility.

James Kwantes is the editor of Resource Opportunities, a subscriber supported junior mining investment publication. Mr. Kwantes has two decades of journalism experience and was the mining reporter at the Vancouver Sun. Twitter: @JamesKwantes

Founder Lawrence Roulston

Resource Opportunities (R.O.) is an investment newsletter founded by geologist Lawrence Roulston in 1998. The publication focuses on identifying early stage mining and energy companies with the potential for outsized returns, and the R.O. team has identified over 30 companies that went on to increase in value by at least 500%. Professional investors, corporate managers, brokers and retail investors subscribe to R.O. and receive a minimum of 20 issues per year. Twitter: @ResourceOpp

Underground drilling

Underground drilling IDM Mining CEO Rob McLeod points toward the mill/tailings facility location in the Bitter Creek Valley.

IDM Mining CEO Rob McLeod points toward the mill/tailings facility location in the Bitter Creek Valley.

Lost Valley gold mineralization

Lost Valley gold mineralization

James Kwantes is the editor of Resource Opportunities, a subscriber supported junior mining investment publication. Mr. Kwantes has two decades of journalism experience and was the mining reporter at the Vancouver Sun. Twitter:

James Kwantes is the editor of Resource Opportunities, a subscriber supported junior mining investment publication. Mr. Kwantes has two decades of journalism experience and was the mining reporter at the Vancouver Sun. Twitter:  Resource Opportunities (R.O.) is an investment newsletter founded by geologist Lawrence Roulston in 1998. The publication focuses on identifying early stage mining and energy companies with the potential for outsized returns, and the R.O. team has identified over 30 companies that went on to increase in value by at least 500%. Professional investors, corporate managers, brokers and retail investors subscribe to R.O. and receive a minimum of 20 issues per year. Twitter:

Resource Opportunities (R.O.) is an investment newsletter founded by geologist Lawrence Roulston in 1998. The publication focuses on identifying early stage mining and energy companies with the potential for outsized returns, and the R.O. team has identified over 30 companies that went on to increase in value by at least 500%. Professional investors, corporate managers, brokers and retail investors subscribe to R.O. and receive a minimum of 20 issues per year. Twitter: