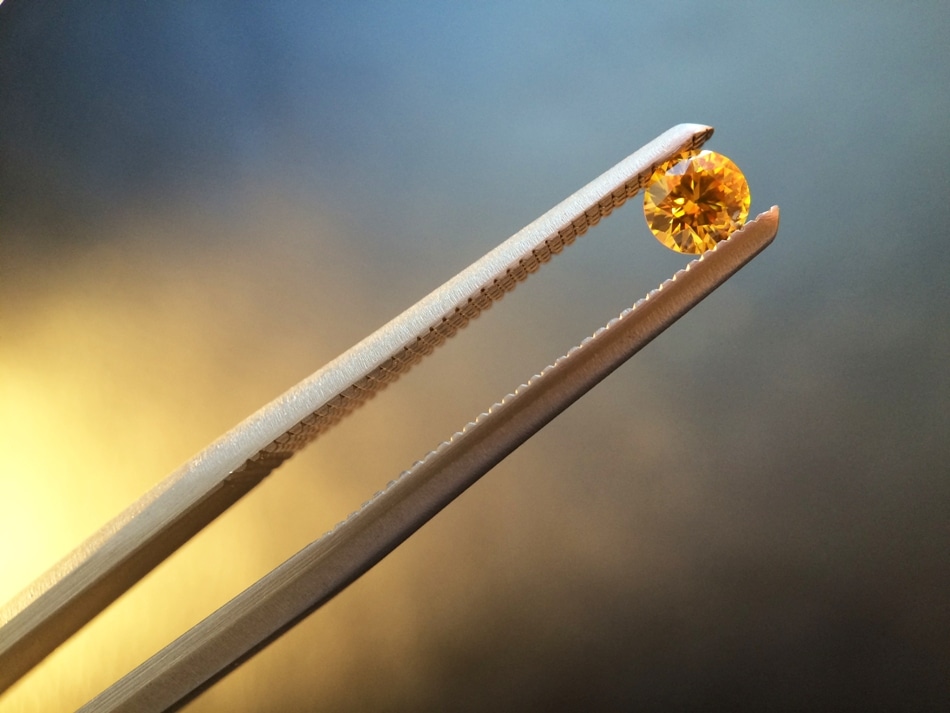

Serendipity – the occurrence and development of events by chance in a happy or beneficial way.

The German pilot who survived a remote plane crash and stayed alive during an Arctic winter by eating a dead passenger. A Yukon pioneer who joined the gold rush with her dad and still lived in the log cabin she and her husband had built in 1910. And a young baritone named Tom Woodward, aka Tom Jones, just before he became an international singing sensation.

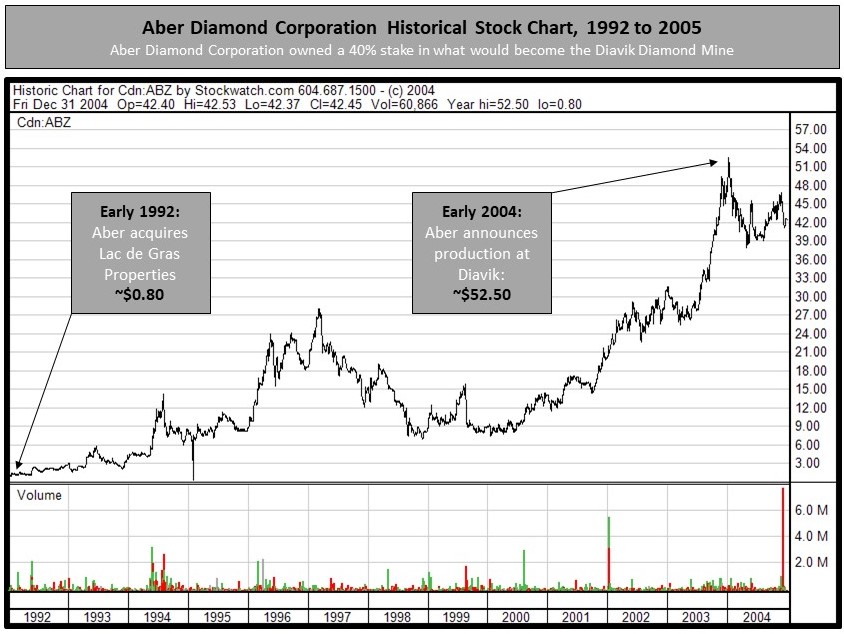

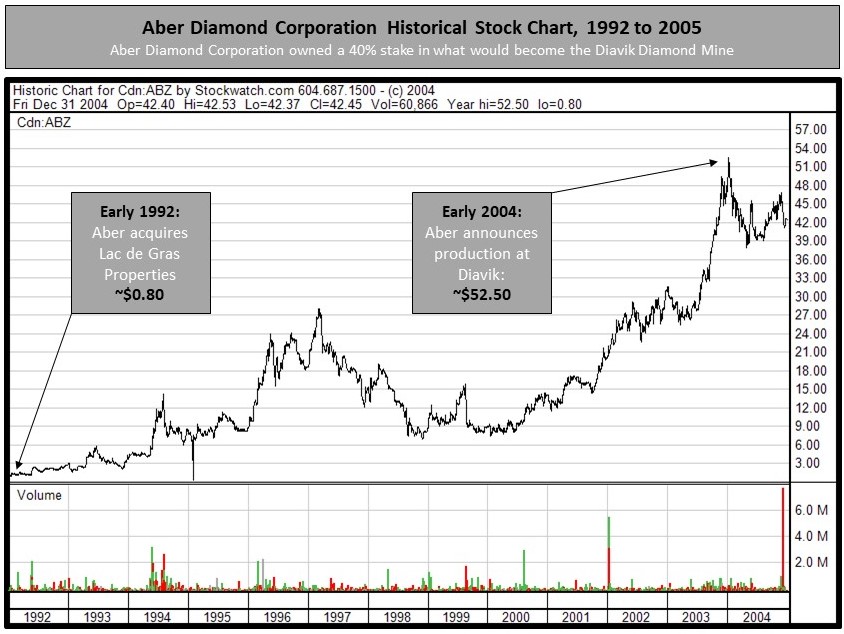

We meet each of these colourful characters and more in the pages of Gren Thomas’s memoir, Serendipity: From Coal Dust to Diamonds, the Adventures of My Life. Thomas left his native Wales for Canada in 1964 and quickly got bitten by the exploration bug. He spent much of the next 30 years bouncing around Canada’s North in helicopters and small planes, and living in remote exploration camps. In 1994, Thomas’s Aber Resources made the Diavik discovery, which became Canada’s second diamond mine.

A sense of wide-eyed wonder pervades Thomas’s book and it’s no surprise. As a young boy, he enjoyed reading books about faraway adventures, before his life became one. From playing cowboys and Indians with pals on the streets of small-town Wales to working closely with First Nations explorers in remote northern Canadian work camps.

The mining entrepreneur, shown below at the Diavik mine opening, grew up in a working-class Welsh mining town. Men followed their fathers and grandfathers into the coal mines and steel mills and tinplate factories. Thomas’s rugby-playing father started working full-time at age 13. His grandfather had signed his dad’s birth certificate with an X.

Thomas’s fate diverted him to university in Cardiff (mining engineering), then to Canada. His first job was surveying underground at Falconbridge’s nickel mine in Sudbury, Ontario, followed by a gig at the Giant gold mine in Yellowknife. Then opportunity knocked.

The wife of a company exploration geologist had run off with the pizza boy, with the geologist in hot pursuit. The vacancy was filled by Thomas, who flew off to his first posting just south of Lac de Gras in the Northwest Territories. It’s now a storied diamond district but Thomas was prospecting for copper.

As he puts it on Page 5, “Things just happened to me. Luck, chance, serendipity — call it what you will — has always played a powerful role in my life. Not that I’m particularly lucky. But just as the three princes of Serendip would chance upon some fortunate happenstance, I would look for one thing and something else quite unexpected would arise.”

Serendipity is a very personal memoir, and the early years were pretty interesting, too. His was a “free range” childhood where getting home before dark was the primary consideration. He and his pals explored quarries, got into mischief and swam in the river. One of his neighbours, the Halls, had a daughter named Jeannie who used to play barefoot in the street as a young child. She later moved to England and married pro soccer player John Nash; their son is Canadian basketball superstar Steve Nash, the Vancouver Whitecaps co-owner and Brooklyn Nets coach.

In 1967, after the two mine gigs, Thomas and three friends went into the exploration business. Two of his partners were Irish and one was an Englishman, so they called the company Anglo Celtic Exploration. Yellowknife was their home base.

Thomas almost didn’t survive that first job. Anglo Celtic was hired by two Vancouver prospectors to stake claims in the remote Nahanni Valley, near the NWT-Yukon border. It was known as the Headless Valley because several prospectors had gone missing and their headless bodies found over the years.

Thomas and his crew flew in on a float plane and landed on the river; they were using two small helicopters to stake. One day, the pilot was preparing to land on the rocky ridge of a razorback high above the valley bottom when the helicopter stalled; the crash landing ripped off both pontoons. The helicopter teetered, then plunged over the edge and began descending to the valley floor. The pilot finally got the engine started and landed on a sandbar in the river.

The plane that was supposed to pick them up after the staking operation couldn’t land because the river was so full of ice. The crew crammed into the two small helicopters, with their gear, and set off through the canyon until it became too dark to fly. They landed on a sand spit and set up for the night. “We huddled that night under an old tarp pitched on the sand, lying there listening to the big ice floes crashing down the river on either side of us.”

The brush with death was a bit of foreshadowing. “Death, it seemed, was never very far away,” he writes. Thomas lost several friends and acquaintances in the North: to drowning, in plane crashes, to murder.

Death, it seemed, was never very far away.

Geologically speaking, there were also plenty of close calls, as well as successes beyond diamonds. Thomas’s Highwood Resources discovered the Thor Lake rare earths deposit, now a feasibility-stage project (Nechalacho) being advanced by Avalon Advanced Materials. Thomas crossed paths with a fascinating cast of characters in the North. Some of the encounters were more consequential than others, of course.

“I met (Chuck) Fipke once in Yellowknife in 1991. I was in the bar of the Explorer Hotel with an English geologist friend, Nigel Hawthorn, and Nigel introduced us. At that time, I didn’t have a clue who he was. The bar was noisy, and Fipke seemed more interested in the stripper, who was gyrating halfheartedly around a pole, than in talking to me.

“That meeting was September 11, 1991. I didn’t know it then, but Fipke had hit the kimberlite motherlode two days earlier at Point Lake, and was on his way back to his Kelowna lab to analyze his samples. When he did, he found microdiamonds.

“The world for me — and the mining industry in Canada — was about to change.”

Fipke’s Dia Met discovery at Lac de Gras, announced in November 1991, set Thomas off on another adventure of a lifetime — one described in the book’s final chapter. Thomas’s group, already very familiar with the area, contacted South African diamond veteran Chris Jennings, who convinced them of the find’s significance. Jennings was in London and jumped on the next plane to Canada.

Speed and secrecy were critical. Thomas and Jennings flew to Yellowknife, separated at the airport and checked in at different motels. They staked well over a million acres of ground that winter, first movers in the world’s largest staking rush. Aber’s Diavik discovery came in the spring of 1994. Some of that ground remains in North Arrow Minerals’ property portfolio.

The Aber Diamond score made Thomas and Aber shareholders a pile of money. Some of his winnings went towards opening the Red Lion Bar & Grill, an old-style U.K. pub, in West Vancouver. It’s named for the pub where one of his grandmothers was born in his hometown of Morriston, Wales.

As for that first company Thomas incorporated, it still exists. Anglo Celtic is the holding company through which Thomas owns large stakes in North Arrow Minerals, B.C. gold play Westhaven Gold and U.K.-focused tin/copper play Cornish Metals.

North Arrow is now processing a partner-funded 2,000-tonne bulk kimberlite sample from its Naujaat project at the Saskatchewan Research Council lab in Saskatoon. The large diamond deposit, located on tidewater in Nunavut, hosts a distinct population of fancy, potentially high-value orangey yellow diamonds. The purpose of the bulk sample is to determine the size profile and quality of the coloured diamond population.

Thomas owns more than 12.9 million North Arrow shares, about 10.7% of the company. Other major shareholders are Lukas Lundin, Ross Beaty and Electrum Strategic Opportunities Fund (Thomas Kaplan), each of which own more than 9% of outstanding shares.

Disclosure: James Kwantes was compensated by North Arrow Minerals for writing this article and owns shares of North Arrow and Westhaven Gold. This article is for informational purposes only and should not be taken as investment advice. All speculators need to do their own due diligence.

Trade and the resulting prosperity set the stage for the tulip bulb mania of the 1630s. Businessmen who became wealthy buying shares in the Dutch East India Company would decorate their estates with lavish flower gardens of tulips, which had been introduced from Turkey. The rarest and most valuable tulips were the ones with genetic impurities, which produced vibrant colours and unique patterns. Human beings love natural beauty.

In diamonds as in tulips, the rarest and most beautiful are the most valuable. Lucara Diamond Corp. (LUC-T) has been demonstrating it for years, pulling spectacular stones out of its Botswana diamond mine and selling them for prices as high as US$63 million. That price-tag, for the 813-carat Constellation, was more than Lucara paid for a controlling interest in the Karowe project before it became a mine. Fancy pink diamonds from Rio Tinto’s recently closed Argyle diamond mine in Western Australia also command high prices.

Human beings love natural beauty. It’s something of a counterpoint to the narrative that De Beers created the demand for diamonds with its legendary “A Diamond Is Forever” advertising campaign in the late 1940s. That branding certainly introduced diamonds to new markets, such as Japan, and established mass market appeal for diamond engagement rings. Natural diamonds, of course, have been objects of desire for thousands of years.

In diamonds as in tulips, chemical impurities create the vibrancy and colour. Fancy diamonds fetch higher prices because the stones are rare and because they are beautiful. The presence of nitrogen, for example, is what gives a population of diamonds from North Arrow Minerals’ (NAR-V) Naujaat project in Nunavut their vibrant orangey-yellow hue.

STAGE SET FOR A DIAMOND REBOUND

The staying power of natural diamonds has been challenged by everything from lab-grown stones to changing demographic trends to COVID-19. It’s been a rough ride for investors in Canadian diamond stories, too — Dominion Diamond Corp. and Stornoway Diamond Corp., operators of two of Canada’s diamond mines, were both forced into bankruptcy protection.

North Arrow has not been spared. The stock has mostly been in the penalty box since a disappointing 2015 valuation of a 383.55-carat parcel of Naujaat diamonds. The primary conclusion of the valuation was that results and modelled values should be treated with considerable caution because of the small size of the sample. North Arrow has cost-effectively advanced Naujaat and its other Canadian diamond projects since, with successes including the discovery of new diamondiferous kimberlite fields at Pikoo (Saskatchewan) and Mel (Nunavut). While other diamond explorecos went bust or switched commodities, North Arrow shed non-core assets, sold small royalties on secondary projects and did modest raises with help from its billionaire backers.

As the world slowly emerges from the pandemic’s grip and consumers from their homes, natural diamond prices and sales are bouncing back strongly. Rough diamond prices have rebounded and recently eclipsed pre-pandemic levels, reports New York diamond analyst Paul Zimnisky in the February 2021 edition of his State of the Diamond Market. De Beers just raised prices at its third consecutive sale, according to Bloomberg.

Sethunya

The pandemic appears to have created pent-up demand for jewelry and diamonds. Tiffany & Co., the world’s largest jeweller, reported record sales for the November 1 through December 31 holiday period. China is leading the way, as the growing consumer powerhouse leaves COVID-19 in the rear-view mirror. Tiffany’s Chinese sales rose 50% during the holiday period. Richemont, the world’s second largest luxury conglomerate, said Q4 sales in China surged 80% year-over-year (Richemont is the parent company of Cartier and Van Cleef & Arpels). Chinese jeweller Chow Tai Fook opened 286 net new stores in the country in the fourth quarter of 2020.

Large diamonds and rare coloured diamonds are leading the way. Last year Louis Vuitton, the world’s most powerful luxury brand and the recent acquirer of Tiffany & Co., purchased two of Lucara’s most prized diamonds — the 1,758-carat Sewelo and the 549-carat Sethunya (right) — with plans to turn them into brilliant centerpieces. The Sewelo is the second largest rough diamond ever mined. A 59.6-carat fancy pink diamond, the “Pink Star,” sold for a record US$71.2 million in 2017.

ENTER THE AUSSIES

Smart contrarian investors are taking notice. One is Michael O’Keeffe, an Australian entrepreneur who has made shareholders lots of money in coking coal and iron ore. A metallurgist by training, O’Keeffe got his start at Mt. Isa Mines and Glencore Australia before launching his own ventures. O’Keeffe took Riversdale Mining, a $7-million Australian coal junior with assets in Mozambique, to a $3.7-billion buyout by Rio Tinto in 2011.

O’Keeffe (right) settled on diamonds after scouring the investment landscape for contrarian opportunities. He teamed up with diamond veteran Peter Ravenscroft, who was independently forming a strategy to consolidate the diamond project development space. They formed Australian-listed Burgundy Diamond Mines (BDM-AX), which plans to become a mid-cap diamond producer by developing premium projects that have been overlooked and/or under-funded.

In June, Burgundy signed a JV deal with North Arrow Minerals (NAR) that will see Burgundy earn a 40% stake in Q1-4 by funding a $5.6-million bulk sample of 1,500 to 2,000 tonnes at Naujaat, North Arrow’s coloured-diamond project in Nunavut. Burgundy advanced $300,000 of that last year so North Arrow could ship fuel and sampling supplies to Naujaat on the annual sealift. The objective of the bulk sample is to confirm that the more valuable coloured diamonds occur in larger sizes throughout the deposit.

The favourable JV deal allows North Arrow to retain majority control of Naujaat on a partner-financed path and established timeline. It undoubtedly helped that North Arrow CEO Ken Armstrong cemented a relationship with Peter Ravenscroft, Burgundy’s Managing Director and CEO, while the latter was in charge of resource delineation at the Diavik diamond mine in NWT. Ravenscroft is a diamond veteran with 40 years in the industry including with De Beers, Anglo American and Rio Tinto.

So what is Burgundy buying into? Naujaat’s Q1-4 kimberlite hosts Canada’s largest undeveloped diamond resource 100% held by a junior. The deposit hosts an estimated 26.1 million carats (Inferred) from surface to a depth of 205 metres; 2017 drilling showed Q1-4 extends below 300 metres depth. The outcropping kimberlite has a distinct population of rare orangey-yellow diamonds that could drive the value proposition and make the deposit economic. The Q1-4 deposit is seven kilometres from tidewater, near the community of Naujaat.

If this summer’s bulk sample is successful, Burgundy could earn an additional 20% interest in Q1-4 (60% total). North Arrow and Burgundy have a non-binding letter of intent to negotiate a second option agreement giving Burgundy the right to earn the additional 20% interest by paying for collection of a subsequent 10,000-tonne bulk sample.

The purpose of that exercise would be to definitely answer the diamond value question. The price tag for that bulk sample would be much higher, too — in the order of roughly $20 million.

SIZE MATTERS. SO DOES SATURATION

Intriguingly, the fancy orangey-yellow diamonds tend to be larger than the other diamonds in Q1-4. The coloured diamonds are a distinct, younger population of stones. In earlier samples taken by North Arrow, they made up between 9-12% of the stones but as high as 21 to 30% by carat weight. Establishing the size-frequency distribution of that fancy diamond population is the main objective of this summer’s 1,500 to 2,000-tonne bulk sample.

High-quality diamonds that are saturated in colour can sell for multiples of the price of white diamonds, but the mines producing them are shutting down. The latest is Rio Tinto’s Argyle mine in Australia, the world’s primary source of fancy pink stones. Argyle closed last year. The Ellendale mine, also in Australia, produced 50% of the world’s fancy yellow diamonds and was Tiffany’s primary supplier for those stones. Ellendale closed in 2015 (although another company is attempting to revive the project).

There were some initial doubts that the Naujaat fancy coloured diamonds would cut and polish well. North Arrow addressed those concerns with its cutting and polishing exercise that yielded beautiful, valuable stones. The polished diamonds received favourable certifications by the GIA (Gemological Institute of America). The diamonds were certified by GIA as fancy vivid orangey yellow — fancy vivid diamonds have the highest colour saturation and command premium valuations.

TOP TEAM, LOW PRICE

In the notoriously risky junior mining sector, investing with people who have track records of making investors money greatly increases the odds of success. Gren Thomas, North Arrow’s chairman and a Canadian diamond pioneer, fits the bill.

On the heels of Chuck Fipke’s September 1991 diamond discovery, Thomas and South African diamond expert Chris Jennings (now a North Arrow director) headed north on a cloak-and-dagger staking mission. They flew into Yellowknife and split up at the airport, staying at different cheap hotels as they systematically staked as much prospective ground as possible.

“We got the feeling that the town was just trembling on the verge of a staking rush,” Thomas recalls. “At any minute, the whole place could blow wide open.”

That winter staking adventure eventually yielded the Diavik diamond discovery and Thomas’s Aber Diamond Corp. (40% owner) saw the rich mine through to production. That worked out rather well for shareholders.

Thomas owns 11.1% of North Arrow’s shares and recently increased his position by loaning the company $400,000. Jennings, his old staking partner, owns a 5.3% stake in North Arrow. Gren’s daughter Eira Thomas led the field exploration team that made the Diavik discovery leading to Canada’s second diamond mine. She co-founded both Stornoway Diamonds and Lucara Diamond Corp. and now runs Lucara, the world’s premier producer of large, high-quality diamonds. Eira is a North Arrow advisor and large shareholder who was key to securing Naujaat for the company. CEO Ken Armstrong is a 25-year veteran of the diamond space and has been involved in the discovery of 10 diamond-bearing kimberlites in Canada and Greenland.

Through Burgundy, O’Keeffe joins three billionaire backers who are involved with North Arrow. Mining tycoons Lukas Lundin (through Zebra) and Thomas Kaplan (Electrum) each own 10.3% stakes in North Arrow; Ross Beaty owns 8.8% of shares. All three put money into North Arrow’s last financing; insiders and key shareholders hold more than 53% of North Arrow’s shares.

A VALUATION GAP

There aren’t many active junior exploration companies backed by the likes of Lundin, Beaty and Electrum that trade below a $15-million market cap. And that’s not the only metric that suggests North Arrow shares are fundamentally undervalued at these levels.

Eira Thomas (left) and Gren Thomas (right) at the Diavik mine opening.

Consider the discrepancy in market capitalization between North Arrow and its JV partner, ASX-listed Burgundy Diamonds. The Naujaat diamond project is the recognized flagship for both companies; after this summer’s bulk sample, North Arrow will own a 60% interest in Naujaat and Burgundy a 40% interest. Yet consider the market cap comparison between joint venture partners:

North Arrow Minerals 60% stake in Naujaat (flagship) Canada’s best portfolio of advanced diamond exploration projects 100% share in Hope Bay Oro, a gold project adjacent to Agnico Eagle’s Hope Bay mine Market cap: C$12.2 million

Burgundy Diamond Mines 40% stake in Naujaat (flagship) Exploration alliance in Botswana Nanuk, an early-stage diamond project in northern Quebec Legacy Peruvian gold/silver asset (25%) Market cap: C$76.9 million

A GOLDEN CALL OPTION

North Arrow’s 4,103-hectare Hope Bay Oro property is three kilometres north of the Doris gold mine — the first to go into production at Hope Bay — and adjacent to Agnico ground. Oro hosts the same rocks, the same structural setting and the same mineralization style as Doris, where gold grades are about 10 g/t Au.

A 1,225-metre drill program completed by North Arrow in 2011 confirmed near-surface, high-grade gold mineralization over 300 metres of strike.

Ten of the 11 drill holes along the Elu shear hit significant gold grades, including:

7.55 metres grading 4.91 g/t Au from 38.4m, including 4.2 metres grading 8 g/t Au;

2 metres grading 20.22 g/t Au from 125m;

4 metres grading 7.04 g/t Au from 42.6m;

1.45 metres grading 31.92 g/t Au from 43.55m.

Acquiring Hope Bay Oro seems to be a logical bolt-on for Agnico, especially given the gold miner’s renewed focus on exploration. Selling it could provide North Arrow with a non-dilutive source of funds. North Arrow CEO Armstrong is evaluating next steps at the property, including a potential drill program.

A BEAUTIFUL FUTURE?

The bet on North Arrow is that 60% or even 40% of a diamond mine that produces valuable fancy diamonds would be worth multiples of the current market capitalization. North Arrow has a partner-funded path to determine if Naujaat hosts an economic diamond deposit sweetened by a population of valuable fancy orangey-yellow diamonds. The JV partner is top-shelf, with the financial backing to fast-track a mine into production.

A final word on tulips and diamonds. Contrary to popular belief, the speculative tulip bubble occurred primarily among a small number of Amsterdam businessmen who had grown wealthy from maritime trade. The tulip bulb trade was considered too speculative for the Amsterdam stock exchange, which was well-established by that time. As spectacular as the 1636-37 tulip price collapse was, it did not affect many Dutch citizens or even have ramifications for that small country’s economy, let alone the world. This was a niche phenomenon.

The appeal of diamonds, on the other hand, spans the globe. While America remains the dominant market, fast-growing and populous countries such as China and India are taking their place on the diamond center stage. Rising tides of prosperity have brought luxury consumer purchases within reach.

Human beings still love natural beauty. That bodes well for fancy coloured diamonds and the companies that can bring deposits hosting those stones into production. The quality of the Naujaat fancy diamonds, the strength of the North Arrow and Burgundy teams, and the recent rebound in diamond sales says North Arrow may be closer to that objective than its market capitalization suggests.

North Arrow Minerals (NAR-V) Price: 0.11 Shares outstanding: 111.68 million (166.4M fully diluted) Market cap: $12.17

DISCLOSURE: James Kwantes owns North Arrow shares and was compensated by North Arrow Minerals for the writing and distribution of this article. This article is presented for informational purposes and is not financial advice. All investors need to do their own due diligence or consult an investment advisor.

October 26, 2018

It’s 1:15 p.m. on a sunny Friday afternoon in Vancouver and I arrive a little early for a downtown meeting with Westhaven Ventures (WHN-V) chairman Gren Thomas. A short elevator ride at Granville and West Hastings takes me to Westhaven’s modest offices on the 10th floor, where I let myself in and drop by CFO Shaun Pollard’s office.

Inside, Pollard and veteran geologist Ed Balon — Westhaven’s technical director — are talking rocks and stocks. Westhaven shares rose 36% on the day to an all-time high close of 94 cents. Teamwork: Balon was key to identifying the Spences Bridge epithermal gold belt, which hosts Shovelnose, outside of Merritt, and Westhaven’s other projects: Prospect Valley, Skoonka and Skoonka North. Pollard runs a tight treasury ship in a sector with its share of (adrift) lifestyle companies.

And it’s at Shovelnose where a high-grade intercept of 17.77 metres of 24.50 g/t gold in hole 14 sent Westhaven shares — which traded between one and three nickels for years until this spring — rocketing from 37 cents to 81 cents on Oct. 16. This is a junior mining market where momentum flows to companies that can hit rich intercepts of high-grade gold. Westhaven has become one of them.

Visible gold in hole 14, from the South Zone at Westhaven’s Shovelnose project

Gren arrives at the office. The soft-spoken mine finder made his reputation and fortune when his Aber Resources discovered Diavik, Canada’s second diamond mine. But these days, it’s mostly gold on his mind.

He comments with a chuckle that he’d had a nap earlier in the day and been surprised when he awoke to see the large stock increase. Making a few million dollars while he slumbers … that’s the new normal for Thomas, who owns (directly and indirectly) almost 30% of Westhaven’s shares. But it’s not like he’s sitting around counting his winnings — the veteran prospector was uncertain and low-balled his stake in the company when asked about it.

Take Resource Opportunities for a test drive and profit from under-the-radar investment ideas before they go mainstream. Use coupon code “CEO” to collect US$100 in savings and subscribe for one year at US$199 (regular $299) or for two years at US$349 (regular $449). Subscribe today!

The Westhaven surge is a reversal of fortune for Thomas, who got his share position by bankrolling the company, keeping it afloat through years of struggle and shoestring budgets. Thomas is Westhaven’s chairman and his son Gareth runs the company as president and CEO. Gareth, who was out of the office for interviews, owns 3.3 million shares, a 4.2% stake.

“What are we going to do with all this paper, paper the walls?” Gren says, recalling earlier days of backstopping the operation.

He fills me in on the small, persistent band of believers who were convinced there was high-grade gold at Shovelnose. Central to early-stage exploration was Balon, who discovered Skoonka and found a boulder at Shovelnose in the mid-2000s that ran 100 g/t gold. That was while both projects were still in Strongbow Exploration (SBW-V), where Thomas is also chairman. A 50-metre intercept of 0.5 g/t gold provided further encouragement.

Shaun Pollard, Westhaven CFO (left to right), technical director Ed Balon and CEO Gareth Thomas, atop Shovelnose.

“There were a lot of small programs, but frustrating. We would go back every year thinking we would find more the next year. But we were basically prospecting with a drill. There is lots of cover there, right.”

“We were talking to major companies and they were not remotely interested.”

Westhaven chairman Gren Thomas

The majors are interested now, and so are plenty of others. Gren’s cellphone rings in the pocket of his jacket, which is draped over a chair. He apologizes for pausing the interview and walks over to take the call. It’s Peter Brown, the Canaccord cofounder and Howe Street legend — and Westhaven shareholder. Brown, too, is eager to know when assays for hole 15 will arrive (anytime) and when the next drilling starts (early November).

Hole 14 was the intercept that lit a fire under Westhaven shares. Hole 15, 100 metres southeast of 14, hit a 20-metre quartz vein and contains visible gold. Assays are pending and could land at any time. The core for hole 14 contains ginguro bands, a distinctive black sulphide that is sprinkled with visible gold. The latest core looks very similar to the mineralization at Hishikari (Sumitomo), a Japanese gold mine with some of the world’s highest grades, at 40 g/t gold. Exploration manager Peter Fischl also sees parallels to Kupol (Kinross), a large high-grade mine in Russia’s Far East. Both Hishikari and Kupol are world-class epithermal gold deposits. Shovelnose is a speculative, earlier-stage project, but the potential is tantalizing.

A turning point, Gren relates, was when exploration manager Peter Fischl — attempting to zero in on the “heat zone” — targeted a valley with a creek that hosted heavy clay alteration. Hole SN17-06 intersected 85 metres of 0.52 g/t Au. Higher-grade intercepts followed earlier this year, including 17.7 metres of 3.9 g/t Au.

“We still couldn’t get any interest. We’ve got the boulders, we’ve got the showings, we’ve got these intersections — there’s a lot of gold here.”

“One company even went so far as to say, ‘There are no mines here. Why are there no mines?’ ”

“Well, because nobody has found one yet,” Gren says with a laugh.

Westhaven Ventures (WHN-V) Price: 0.94 Shares outstanding: 85 million (92 fully diluted) Market cap: $80 million

There are also new developments in the other two companies where Gren is chairman: Strongbow Exploration (SBW-V) and North Arrow Minerals (NAR-V). He is preparing to fly to the U.K. with Strongbow CEO Richard Williams to work on fundraising and an AIM listing for Strongbow, which is developing the high-grade South Crofty tin project in Cornwall. An Oct. 17 deal with Orion Mine Finance should help on that front — the well-known mining group agreed to finance Strongbow to the tune of US$3 million in conjunction with the AIM listing, which is expected before the end of the year. Thomas owns 5.133 million Strongbow shares, a nearly 6% stake.

There are large pools of capital in London for U.K. mining projects, which Williams and Thomas plan to tap into. There is also renewed interest in Cornwall and tin mining thanks to a popular British television series called Poldark. One participant in a recent tourist walking tour of Cornwall turned out to be a fund manager who was interested in Strongbow and South Crofty.

Strongbow is the “mother ship” of Gren’s three companies: diamond play North Arrow Minerals was spun out of Strongbow in 2007 and Westhaven optioned its Spences Bridge gold belt properties from the company. The deals for Shovelnose and Skoonka have left Strongbow with a 2% royalty on Shovelnose as well as 3.1 million Westhaven shares. Those shares are now worth almost $3 million — a not-insignificant total for a company with a market capitalization of about $14 million. “It’s funny how things morph,” Thomas remarks of Strongbow’s pivot from gold to tin.

Strongbow has a mining permit that is valid until 2017 and the company is currently building a dewatering plant to treat water from the old mine workings. The project was financed by the $7.17-million sale of a 1.5% NSR to major shareholder Osisko Gold Royalties, which owns a 27.5% stake.

Strongbow Exploration (SBW-V) Price: 0.16 Shares outstanding: 86.6 million (127.4M fully diluted) Market cap: $13.9 million

As for North Arrow Minerals, the diamond play is awaiting microdiamond and till sample results from Mel in Nunavut, where it discovered the diamondiferous ML-8 kimberlite last year. This season North Arrow drilled a new kimberlite (ML345), expanded on ML-8 and collected 224 kg of kimberlite for microdiamond analysis.

Cut and polished fancy yellow-orangey diamond from Naujaat.

One of the main focuses of North Arrow CEO Ken Armstrong is getting a road permitted from the town of Naujaat to the Q1-4 kimberlite, which hosts a population of valuable yellow-orangey diamonds.

Completion of a road would dramatically cut the costs of collecting a large bulk sample to get a better sense of diamond values at the 12.5-hectare kimberlite, which is near tidewater. A road to the community, which is very supportive of the idea, would also potentially allow the construction of a small test mill in Naujaat.

“A major should take this on, because they take a longer-term view of it,” Gren says of Naujaat. “It’s the perfect place for a mine, near the coast.” He owns more than 10.5 million North Arrow shares, an 11.5% stake.

North Arrow Minerals (NAR-V) Price: 0.14 Shares outstanding: 92.8 million (128.9M fully diluted) Market cap: $13 million

“We’re quite confident that we’re doing the right things,” Thomas says of progress at Strongbow and North Arrow. “We just wish the markets would show more interest.”

That’s no longer a problem at Westhaven, with shares sitting just shy of a dollar as investors anticipate assays for hole 15. Warrant exercises have topped up the treasury, which sits north of $1.5 million. That’s enough for the next drill program, which is imminent, and it removes the need to finance under a dollar — something Gren is loathe to do.

While Westhaven’s fortunes have changed, its corporate culture will not, Gren pledges. “Gareth and I were talking about it, and I told him – ‘We under-promise and over-deliver.’ So no bullshit. It’s funner and you get a lot fewer phone calls from angry shareholders.”

There aren’t many of those these days, and Westhaven’s share structure all but ensures higher prices IF the company can keep hitting high-grade gold. Management own about 40% of shares, the Plethora Precious Metals Fund owns 16% and friends and family (including Gren’s daughter Eira Thomas) own another 10-15%. Those high ownership levels keep the supply of shares low during a period of rising demand for the stock.

Disclosure: James Kwantes owns shares of Westhaven Ventures, Strongbow Exploration and North Arrow Minerals and covers each company in his newsletter, Resource Opportunities. North Arrow is a sponsor of the newsletter. This article is for informational purposes only and should not be considered financial advice. All investors need to do their own due diligence.

North Arrow Minerals is 1 of 3 Resource Opportunities sponsor companies.

Vancouver-based North Arrow Minerals is one of the more active diamond exploration companies globally, with a portfolio of projects focused on Canada. Its most advanced-stage project is the large Naujaat deposit in Nunavut, which has a resource and hosts a population of valuable fancy orange yellow diamonds.

But this season’s focus is on exploration drilling at the Mel and Loki projects in Nunavut and the Northwest Territories, respectively. Mel was a grassroots diamond discovery that North Arrow announced late last year. The company traced kimberlite indicator mineral (KIM) trains up-ice and made a prospecting discovery of kimberlite, from which 23 microdiamonds were recovered from a 62.1-kg sample. The first drilling program on the property is planned for this summer.

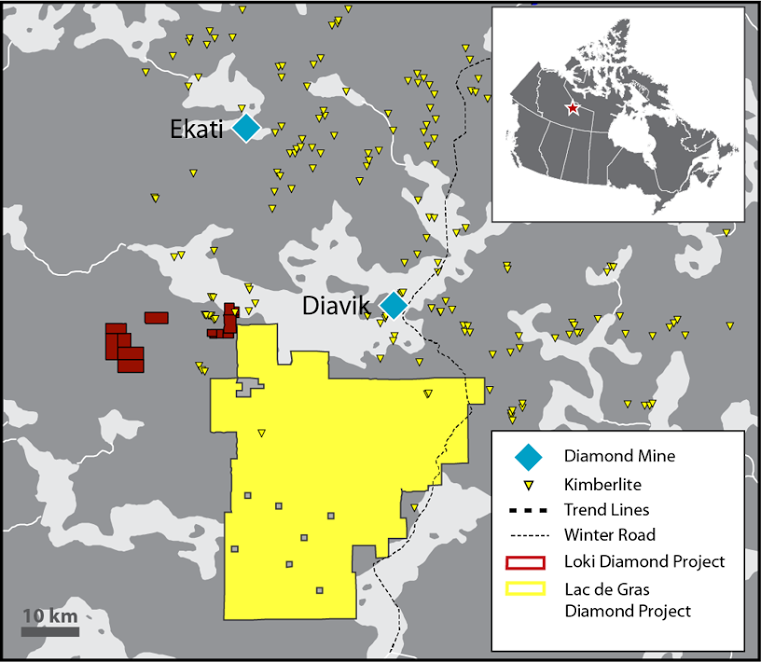

The Loki project is in the Lac de Gras diamond field that hosts the Diavik and Ekati mines. The focus there is EG05, a kimberlite that Rio Tinto discovered, and 465, a kimberlite discovered by North Arrow in the spring. The latter was the first kimberlite discovery in Lac de Gras in the past 5 years. It’s familiar terrain for the North Arrow team, including chairman Gren Thomas whose Aber Resources discovered the Diavik diamond mine.

North Arrow CEO Ken Armstrong

Rough diamond prices are now at a 52-week high and demand for polished diamonds is strong in China, India and the U.S., according to New York-based diamond analyst Paul Zimnisky. On the production side, pending mine closures including Argyle and Victor will put pressure on supply, with few new operations coming online.

The improving picture follows a choppy 2017 that saw high inventory levels at De Beers and Alrosa and flat rough diamond prices. North Arrow shares have been under pressure along with shares of new Canadian producers Stornoway Diamonds and Mountain Province Diamonds, which declined 41% and 18% respectively over the past year as startup problems weighed.

On Monday North Arrow announced a $3-million private placement consisting of flow-through shares at 20 cents and non-flow-through units (one share, one 2-year 30-cent warrant) at 17 cents. We caught up with CEO Ken Armstrong, who was in Calgary for the TakeStock! investor forum, to find out more about plans and how the money will be used.

Q: What is the breakdown on how the $3-million financing will be spent?

A: We’ve allocated $2 million for Mel drilling – testing the 2017 kimberlite discovery and new targets. That number includes microdiamond processing costs. We will also complete microdiamond processing of the EG05 and 465 kimberlites at the Loki project that were drilled in March, as well as some final microdiamond processing from the 2017 drilling of Naujaat. That’ll be a couple hundred grand. We are also looking at getting a remaining top target drilled at Loki, target 853. Ideally we’d tie that onto ongoing drilling at our LDG JV property, which is operated and funded by partner Dominion Diamond. We’d retain a half million or so for G&A.

Q: Any big names buying into the financing? How much will insiders and management participate for?

A: Insiders are committed to taking at least $1.5 million, so half, with most of that being directors/management. Gren Thomas, our chairman, and Eira Thomas, a North Arrow advisor, will both participate. I will also participate.

Q: How did you determine the pricing of the financing?

A: We tried to price it to make the non flow-through unit and flow-through share components equally attractive. On the Unit we put a fairly quick threshold on the accelerator, at 40 cents, however we felt it was justified by pricing it a discount to market with a full warrant, rather than a half-warrant. The flow through is essentially priced at market with the intent to fill the orderbook efficiently. We are looking at immediate use of funds with Mel drilling in July, Loki drilling in July or August and with more diamond results from Loki, Naujaat, and in September or October, from Mel. This is all news flow that will occur before the four-month hold comes off the financing shares which is, we think, a positive feature of the placement. We have been the most active Canadian junior in terms of new kimberlite discoveries in Canada and are poised for more discovery, potentially on up to three projects, over the four months.

The esker location at Mel where North Arrow’s drill camp is being set up.

Q: Which of the three active projects that you’re raising money for is the most likely catalyst — Loki, Mel or Naujaat?

A: All three have potential catalysts. Folks seem to be most interested in new discoveries and Mel certainly fits that bill — it’s a brand new kimberlite discovery made by prospecting last fall. The kimberlite contains some very coarse mantle minerals and we see hints of that coarseness in the initial diamond results, which is positive. Having already found kimberlite and diamonds actually de-risks the initial drilling significantly. We know we will hit kimberlite with diamonds, it’s more a question of how many and how big they are.

Based on the spread of indicator minerals there are certainly multiple sources with some nice, sizable magnetic targets. This is a brand new kimberlite field and the first kimberlite discovered is significantly diamondiferous. It doesn’t happen too often, so we are keen to get drilling. We’re currently mobilizing a camp and drill to the property now with drilling planned for July.

At Loki we also have a new discovery and are waiting on microdiamond results. In early April we announced the discovery of the 465 kimberlite – the first kimberlite discovery made in the Lac de Gras area in over 5 years. There are also pending microdiamond results from the EG05 kimberlite which was also drilled during the spring 2018 program. We also have a number of targets that we’d like to drill test, including target 853, which we’d like to see drilled this summer.

Q: It’s been almost three years since the disappointing Naujaat diamond valuation. Does Naujaat remain North Arrow’s flagship project and what is happening with the project?

A: Naujaat remains North Arrow’s most advanced project. We’re still interested because it’s a significant diamond inventory in a large tonnage deposit (as far as Canadian diamond deposits go) sitting on tidewater near a community. Our work on the Q1-4 diamonds has clearly shown the deposit contains high-value fancy orange yellow diamonds and, overall, is under evaluated. Last summer we completed more drilling to confirm the size potential of the kimberlite down to 300 metres below surface and we had three different holes extend over 100 metres beyond the geological model, with two of those holes ending in kimberlite. It’s a big body. We also collected a 210-tonne sample that confirmed the presence of the coloured diamond population in the A88 phase of the kimberlite. This is a totally different unit than was sampled in 2014 – the 2017 sample pit was over 400 metres away for the 2014 pits – and the proportion of coloured stones is very similar to the 2014 result. The work we’ve done with the diamonds themselves has shown that the coloured stones are a distinct population from the non-coloured stones. The two populations are completely different ages and the yellow population has a markedly coarser distribution than the non coloured stones.

The photos of the diamonds we had polished and certified at the GIA show how beautiful this colour is and highlight the potential value upside in these diamonds. But it is actually the potential for a coarse size distribution that may be even more important in terms of potential upside to the value contribution of the coloured diamonds. And the only way to confirm or disprove the potential value upside is a larger bulk sample.

A cut-and-polished fancy intense orangey yellow diamond from North Arrow’s Naujaat project.

To that end we have hired consultants and been working closely with the community of Naujaat to look at developing a road to the deposit. We’ve also started looking at processing options for a larger sample and how that might look, all with an eye to better pinning down the budget options for collecting a sample of sufficient size to get that answer. Being so close to the community really presents opportunities for reduced costs – we’ve seen that with our exploration programs and we need to make sure we take full advantage of all potential cost savings.

Of course all this takes time, but that is why we have North Arrow evaluating a number of quality projects, not just one. It allows the team to focus on well-informed, cost-effective exploration even if that might mean slower news flow from a particular project. There will be steady news flow from other projects as each cycles through the process.

Q: Along the lines of quiet projects, what is the status of the Lac de Gras joint venture with operator Dominion Diamond Corp.?

A: The LDG JV is having an active year. It has definitely been one of our quieter projects as our partner Dominion spent a lot of effort defining targets through a series of overburden drilling and geophysics programs. Late last year, Dominion also went through a well-documented takeover by the Washington Group of Companies, with the resulting transitions that often accompany such changes. However, a very positive outcome for the LDG joint venture has been Dominion’s renewed commitment to exploration, and, as I understand it, the 2018 LDG JV budget was one of the first budgets approved by the new ownership. The focus of the 2018 program is exploration and discovery-type drilling and we expect that work to pick up again during the summer. North Arrow elected not to finance its share of the current program so we could focus our resources drilling our 100% owned projects at Mel and Loki. However, although we are taking dilution of our joint venture interest, if a Lac de Gras-type discovery is made North Arrow will still maintain a significant interest, north of 25%, in the joint venture.

Q: With Eira recently taking over as CEO of Lucara Diamond Corp., how involved does she remain with North Arrow?

A: Eira’s involvement with North Arrow has been key since we began our focus on the Canadian diamond space. She remains an important advisor and sounding board for management – and the board – as we strategize on how best to move the project portfolio forward.

Disclosure: North Arrow Minerals is one of three Resource Opportunities sponsor companies and James Kwantes owns North Arrow shares. Readers are advised that this article is solely for information purposes. Readers are encouraged to conduct their own research and due diligence, and/or obtain professional advice. The information is based on sources which the publisher believes to be reliable, but is not guaranteed to be accurate, and does not purport to be a complete statement or summary of the available data.

Copyright: This publication may not be reproduced in whole or in part, in any form, without the express permission of the publisher. Permission is given to extract parts of the report for inclusion or review in other publications only if credit is given, including the name and address of the publisher.

North Arrow Minerals is one of three Resource Opportunities sponsors and Lucara Diamond and North Arrow are portfolio companies.

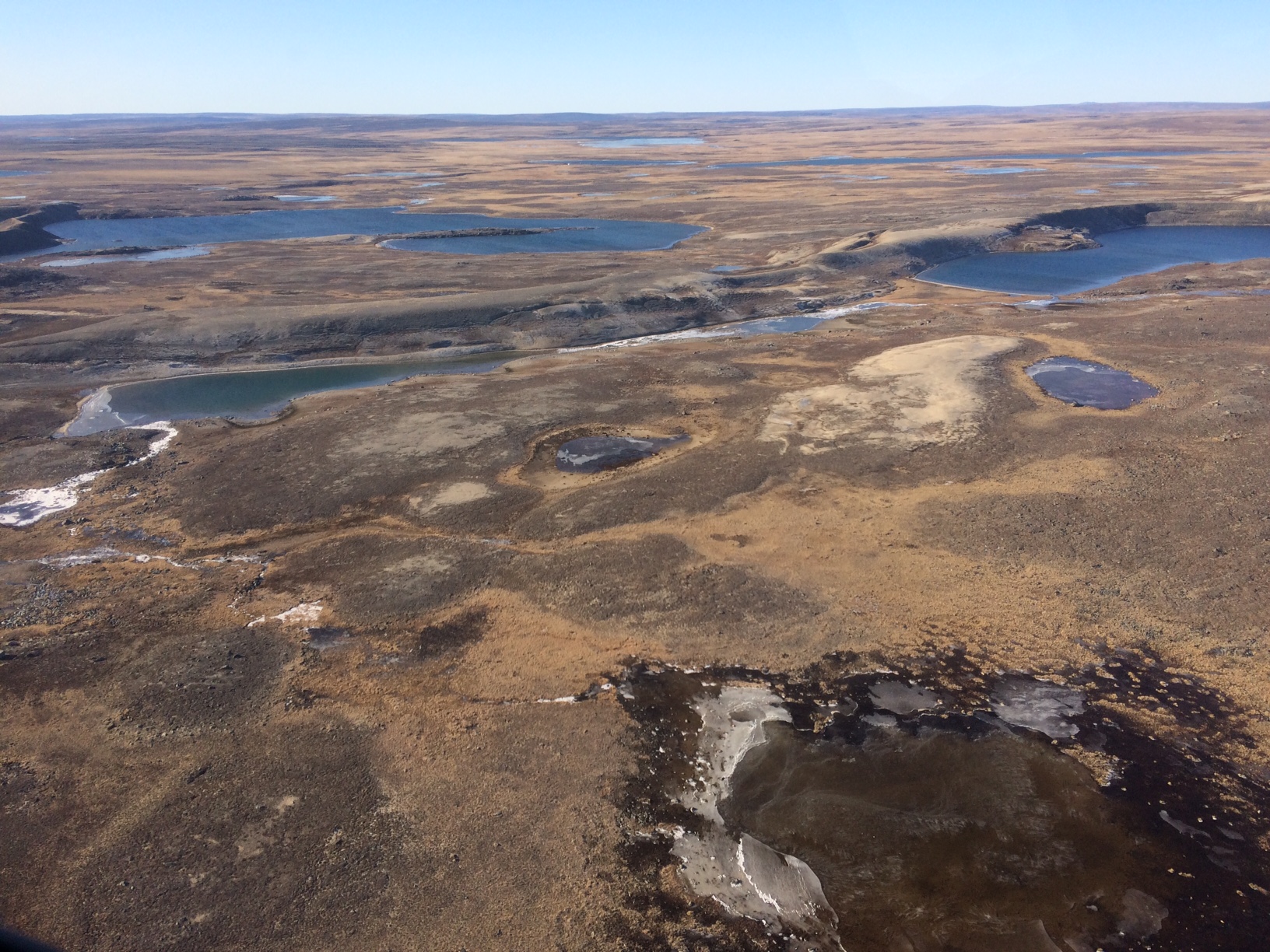

Canada punches above its weight in the world of diamonds – way above. Consider: the country is home to about 36 million people, or less than half of one percent of the world’s population. Yet in 2017, Canada produced 14% of the world’s diamonds by value, behind only Russia and Botswana.

The epicenter of Canadian diamond production lies in the frozen tundra of Canada’s North – the “Barren Lands,” in author Kevin Krajick’s words. Specifically, the Lac de Gras region, 300 kilometres northeast of Yellowknife, the Northwest Territories’ capital city. That’s where prospectors Chuck Fipke and Stu Blusson discovered the kimberlite indicator minerals that let to Dia Met’s 1991 diamond discovery. When Ekati went into production in 1998, it marked the birth of what has become an important northern industry.

The discovery of the Diavik diamond mine by Gren Thomas’s Aber Resources in 1994 established that the Ekati find was no fluke. Diavik went into production in 2003 and quickly became one of the world’s richest diamond mines. The discovery of diamonds in this inhospitable corner of the world, surrounded by only frozen lakes and tundra, is a testament to the ingenuity and perseverance of Canada’s diamond pioneers.

Two decades later, the Ekati and Diavik diamond mines are still churning out carats – and cash. More than $20 billion worth of diamonds has been mined at the two operations. The prized profit centers didn’t escape the notice of the Washington Group, a private conglomerate founded by US billionaire Dennis Washington. Last year the Washington Group paid about US$1.2 billion to snap up Dominion Diamond Corp., owner of a controlling 90% interest in Ekati and a 40% stake in Diavik (operator Rio Tinto owns 60%).

Aerial photo of the Diavik diamond mine, 60% owned by operator Rio Tinto and 40% owned by Dominion Diamonds.

CANADA’S GROUND ZERO FOR DIAMONDS

And the Lac de Gras region remains a hub of activity for diamond production and exploration, well beyond Ekati and Diavik. The newest mine is Gahcho Kue, which began commercial production in March 2017 and is 51% owned by De Beers and 49% by Mountain Province Diamonds (MPV-T).

North Arrow Minerals (NAR-V), Canada’s most active diamond exploreco, is also zeroing in on Lac de Gras. The company has two projects in the region and both of them will see drilling this spring. The Loki project covers 8,600 hectares and is close to both Ekati (33 km away) and Diavik (24 km). North Arrow will drill about 1,000 metres on up to six targets in March.

Loki is a good example of a junior company benefiting from millions of dollars spent by a major while big money flowed into exploration. One of the six Loki targets is EG05, a diamondiferous kimberlite that Rio Tinto (Kennecott) discovered but never followed up on. The other targets were identified through airborne geophysics and electromagnetic surveys. At each target, pyrope garnets and other kimberlite indicator minerals have been recovered, but no source has been found.

At Dominion’s Lac de Gras (LDG) joint venture with North Arrow, operator Dominion is ramping up for 2018 exploration, including spring drilling. Dominion has an approximate 67% interest in LDG, with North Arrow retaining 33%. The LDG JV covers a vast 125,000-hectare property to the south of the Ekati and Diavik mines and immediately east of Loki.

The “privatization” of Dominion Diamond Corp. translates into fewer eyes on the company, particularly its exploration initiatives. But Patrick Evans, Dominion’s CEO – appointed after the takeover – is well-known in the diamond world. Evans is the former president and CEO of both producer Mountain Province Diamonds (MPV-T) and explorer Kennady Diamonds (which was recently taken over by Mountain Province for $176 million).

DRIVE FOR DISCOVERY

Evans’ exploration background – and his assertion that new diamond discoveries are critical to the viability of the Canadian diamond industry – will likely ensure that exploration remains a key focus for Dominion. In a 2016 talk at the annual Roundup Mineral Exploration conference in Vancouver, Evans lamented the “paltry” amount being spent on diamond exploration in Canada. The dearth of exploration threatens Canada’s No. 3 position as a world diamond player, Evans said at the time.

Loki and the LDG joint venture represent North Arrow’s most imminent potential catalysts. But North Arrow continues to advance its flagship Naujaat coloured diamond project in Nunavut, which has a population of rare, valuable fancy yellow diamonds.

On Wednesday the company announced it had recovered 64.25 carats from a 209.8-tonne mini bulk sample collected last year from three phases of the large Q1-4 kimberlite. The proportion of the more valuable yellow diamonds was consistent with an earlier bulk sample – 10.7% of the total by stone count and 21.2% by carat weight.

“It’s encouraging, because it confirms the yellow diamond population exists in different phases of the kimberlite,” said North Arrow CEO Ken Armstrong, noting that the results merit further work. “The size of the prize is large.”

The next step, Armstrong says, is a large bulk sample at Naujaat – perhaps as large as 5,000 to 10,000 tonnes. A sample of that size would answer remaining questions about the value of the diamonds and size-frequency distribution of the yellow stones, he said. It would also carry a large price tag: perhaps between $20 million and $30 million. Securing a joint venture partner would allow North Arrow to undertake the bulk sample without blowing out the share structure, Armstrong pointed out.

Fancy yellows and orangey-yellow diamonds from an earlier sample at North Arrow’s Naujaat.

The diamond sector has faced some ups and downs in recent years, but mostly downs. One of the main issues has been large inventories held by industry heavyweights Alrosa and De Beers, which has suppressed rough diamond prices. There have been some high-profile scandals in the sector, too – Indian diamond magnate Nirav Modi fled India earlier this year and is currently being investigated for alleged bank fraud and money laundering.

However, the macro picture is improving, according to New York diamond analyst Paul Zimnisky. Inventory levels for both De Beers and Alrosa are at estimated three-year lows and demand remains healthy, according to Zimnisky’s latest State of the Diamond Market report. On the supply side, no new mines are coming onstream in 2018 and Alrosa’s production is forecast to decrease this year.

For a sector that has struggled – and been bypassed by many retail investors – there’s a lot going on. The takeover of Dominion Diamond by a private group was a surprise to many; less so the purchase of Kennady Diamonds by Mountain Province, which had earlier spun out the exploreco. There are new and rejuvenated exploration plays, including Bruce Counts’s newly listed Lithoquest Diamonds (LDI-V) with its North Kimberley project in Australia. In the Northwest Territories, GGL Resources (GGL-V) has revamped with the appointment of 25-year diamond veteran David Kelsch as CEO and an injection of capital from project generator Strategic Metals.

ENTER EIRA

But for diamond sector investors, perhaps the most interesting moves were made by Lucara Diamond Corp. (LUC-T) on February 25. Diamond veteran Eira Thomas was named Lucara’s CEO and the Vancouver-based company announced a blockchain initiative that could improve transparency and efficiencies in the sale of diamonds in the one to 15-carat range, and eventually for smaller stones as well. Blockchain will not be used to sell the larger diamonds that have established Lucara’s reputation and bolstered its treasury – stones such as the 1,109-carat Lesedi La Rona and 813-carat Constellation.

Eira’s most recent CEO gig was with Kaminak Gold, which was sold for $520 million to Goldcorp in 2016. Before that, Eira – the daughter of North Arrow chairman Gren Thomas – cofounded Stornoway Diamond Corp. (SWY-T) and Lucara. Her partner on both initiatives was Catherine McLeod-Seltzer, who is joining Lucara’s board of directors. The appointments mark a kind of reunion for Lucara’s three co-founders – Thomas, McLeod-Seltzer and Lukas Lundin.

Lucara Diamond CEO and North Arrow advisor Eira Thomas

But before Stornoway, Lucara or Kaminak was Aber Resources. Hired as an Aber field geologist straight out of university, Eira was thrust into a lead role when a senior geologist left for another company. In the spring of 1994, the geologist and her exploration team raced the spring melt and drilled one final hole from a floating ice platform. The core had a 2-carat diamond embedded in it, and the rest is history. She later became VP Exploration for Aber, Dominion Diamond’s predecessor company.

Eira’s appointment as Lucara CEO strengthens already solid connections between Lucara and North Arrow. She remains a North Arrow advisor and large shareholder, and was critical in landing $2-million investments from both Ross Beaty and the Electrum Strategic Opportunities Fund L.P., which is funding North Arrow’s current programs. There’s a brother connection between the two companies, too – North Arrow CEO Ken Armstrong’s brother John is Lucara’s vice-president, mineral resources. His specialty is the assessment and analysis of diamond size and value distribution as well as deposit modelling. John Armstrong’s partner Allison Rippin Armstrong, a corporate social responsibility specialist, is an advisor to North Arrow.

As for Eira, her association to North Arrow’s flagship Naujaat project runs deep. It was Thomas who secured the Naujaat project (formerly called Qilalugaq) from Stornoway Diamonds and brought it to North Arrow, after stepping down as Stornoway’s executive chairman. The Naujaat, Pikoo and Timiskaming projects were optioned from Stornoway on a JV basis, with North Arrow subsequently buying out Stornoway’s stakes to secure 100% interests in Naujaat and Pikoo.

Collecting the mini-bulk sample at North Arrow’s Naujaat project in Nunavut.

Assays are pending for 2,440 metres of kimberlite core drilled at Naujaat last fall. Further drilling later this spring will conclude the program at the 12.5-hectare kimberlite, the largest in the Eastern Arctic. Naujaat has an Inferred mineral resource of 26.1 million carats from 48.8 million tonnes grading 53.6 carats per hundred tonnes, from surface to 205 metres depth. Fall drilling established that Q1-4 remains open at depth and has a surface area of at least five hectares 305 metres below surface.

Further north, there are also drill plans at Mel, North Arrow’s second grassroots discovery of a diamondiferous kimberlite field in Canada (Pikoo was the first). In October, North Arrow announced the recovery of 23 diamonds larger than the .106-mm sieve size from a 62.1-kilogram sample at the ML-8 kimberlite. The diamond body was discovered through the systematic tracking of a kimberlite indicator mineral (KIM) train to its up-ice termination. North Arrow has subsequently increased its Mel land position to 56,000 hectares through staking. Driling will focus on ML-8 as well as other targets at the heads of three well-defined KIM trains.

Disclosure: North Arrow Minerals is one of three company sponsors of Resource Opportunities and James Kwantes owns North Arrow and Lucara shares, which makes him biased. Readers are advised that this article is solely for information purposes. Readers are encouraged to always conduct their own research and due diligence, and/or obtain professional investment advice. Dollar and $ refer to Canadian dollars, unless otherwise stated.

North Arrow Minerals is one of three Resource Opportunities sponsors.

The November 1991 discovery of diamonds in the Northwest Territories by Chuck Fipke and Stu Blusson put Canada on the global diamond map. It also triggered one of the largest staking rushes in the world, as hundreds of companies hurried north to find treasure.

A few years later, many had retreated to warmer climes. One company that remained in the hunt was Gren Thomas’s Aber Resources, with a large land package staked by Thomas and partners at Lac de Gras near the Fipke find. In the spring of 1994, an Aber exploration crew led by Thomas’s geologist daughter, Eira Thomas, raced the spring melt to drill through the ice in search of kimberlite — the rock that sometimes hosts valuable diamonds.

It was a longshot. Since the Fipke find, the great Canadian diamond hunt had virtually ground to a halt — despite the millions of dollars spent in search of the glittery stones. But the drill core from that final spring hole had a two-carat diamond embedded in it. The Diavik discovery meant it was game on for Aber — and Canada’s nascent diamond industry.

DIAMOND POWER PLAYER

A quarter century after that fateful hole was punched through melting ice, Canada punches above its weight in the world of diamonds. Measured by value, the country is the third largest producer of diamonds by value globally. And the valuable diamonds that continue to be unearthed at the Diavik mine discovered by Aber are a big reason why.

The discovery unleashed a wave of shareholder value. The shares of Aber and its successor companies went from pennies to more than $50 as the quality of the diamonds and the asset became known. Dominion Diamond Corp., as Aber is now known and which owns the Ekati mine and 40% of Diavik, is Canada’s premiere diamond company. Diavik is expected to produce about 7.4 million carats this year, making it among the world’s largest diamond operations.

The team behind the Diavik discovery has also created a fair amount of shareholder value in the years since, led by Eira Thomas. She has co-founded two diamond players, Stornoway Diamond Corp. and Lucara Diamond Corp., and remains a director of the latter Lundin Group company. Her most recent gig, as CEO of Kaminak Gold, ended rather well — Goldcorp bought the company for $520 million last year.

A cut fancy orangey yellow diamond from Naujaat

Thomas is also an advisor to North Arrow Minerals (NAR-V), a cashed-up junior company at the forefront of Canadian diamond exploration. Aber’s Gren Thomas is North Arrow’s chairman and the CEO is Ken Armstrong, a former Aber and Rio Tinto geologist. North Arrow recently raised $5 million to explore its portfolio of projects and a drill program is underway at its advanced-stage Naujaat project, which hosts a population of valuable fancy orangey yellow diamonds.

In a space with few new discoveries or development projects, Canada is home to two of the world’s new diamond mines. Stornoway’s Renard mine in Quebec and Gahcho Kue, a De Beers-Mountain Province joint venture in the Northwest Territories, have both recently begun commercial production.

Globally, the diamond industry has faced headwinds, including India’s demonetization and choppy rough stone prices. But diamonds remain a money maker for some of the world’s largest mining companies, including Rio Tinto (60% owner of Diavik) and Anglo American. Incoming Rio boss Jean-Sebastien Jacques identified diamonds as a “priority area” last year in a Bloomberg interview: “I would love to have more diamonds, to be very explicit.” The company recently backed up those words by signing a three-year, $18.5-million option on Shore Gold’s Star-Orion South diamond project in northern Saskatchewan.

And Anglo’s De Beers division remains a reliable profit generator. In 2016, rough diamond sales surged for both Anglo American (up 36%) and Russian producer Alrosa (up 26%), according to The Diamond Loupe. A recent hostile takeover bid for Dominion Diamond reflects the demand for well-run diamond mines, which are powerful profit machines.

EXPLORATION DEFICIT

The picture is less promising on the exploration front. Budgets dried up during the mining slump that began in 2011, and little grassroots exploration work is being done. It’s particularly problematic for supply because diamond mines take longer to discover, evaluate and build pharm. The new Canadian mines will help fill the gap, but it won’t be enough. Economic diamond discoveries have simply not kept pace with mine depletion, globally.

“There are definitely a lack of new projects, at least new projects that are close to infrastructure,” said Paul Zimnisky, a New York-based independent diamond analyst. “There really is not much at all in the global diamond production pipeline.”

Economic, world-class diamond projects are few and far between, and most exploration companies looking for them have failed, Zimnisky explained. That has resulted in wariness and declining interest among investors: “In general, shareholders have not done well in diamonds.”

The looming supply deficit is particularly acute for rare coloured diamonds, which fetch higher prices. Australia’s Ellendale mine produced an estimated 50% of the world’s fancy yellow diamonds before closing in 2015. The Argyle mine, also in Australia, is one of the world’s biggest mines and a source of valuable coloured diamonds, including extremely rare pinks. It, too, is slated to close in the coming years, after decades of production.

North Arrow’s Naujaat could help fill the void. The project hosts a population of fancy orangey yellow diamonds that are more valuable because of their rarity. Naujaat is on tidewater, which dramatically reduces costs, and hosts a very large diamondiferous kimberlite, Q1-4, that outcrops on surface.

It’s the focus of this year’s $3.2-million program, which will see North Arrow drill 4,500 metres and collect a 200-tonne mini bulk sample. The goal is to extend the Inferred resource to a depth of at least 300 kilometres below surface and better define the diamond population. The sample will be shipped south in late August and processed in the fall.

“There is excellent potential to extend the Q1-4 kimberlite at depth, beyond the reach of past drilling efforts,” said North Arrow CEO Ken Armstrong. “It’s the first drilling in more than 12 years. The work will help us confirm and update the size of Q1-4 and improve our understanding of the deposit’s internal geology and diamond distribution.”

In 2014 and 2015, North Arrow collected a small bulk sample at Naujaat (formerly known as Qilalugaq) with the goal of gauging diamond values. But the carat values on the small 384-carat package came in significantly below expectations. North Arrow shares were relegated to the market penalty box and the company has been largely under the radar since, despite important background work that set the stage for this year’s program.

RISK AND OPPORTUNITY

Contrarian investing and the ability to time cycles can lead to fortunes in the junior mining sector. Vancouver investor Ross Beaty has proven it, time and again. In the early 2000s, with copper trading for under US$1 a pound, his team assembled a portfolio of unwanted copper assets in a bear market. He developed and sold those projects during bull markets, turning $170 million in invested capital into shareholder returns of $1.87 billion. His latest win was a large bear-market investment in Kaminak Gold, later bought out by Goldcorp.

Beaty’s latest contrarian bet is on North Arrow, through a $2-million investment that was part of the recent $5-million private placement financing. Other investors included the New York-based Electrum Strategic Opportunities Fund ($2 million) and company management and directors. The money will fund an aggressive program at Naujaat including drilling and a bulk sample, as well as exploration at North Arrow’s Mel, Loki and Pikoo projects.

North Arrow also has exposure to drilling through the LDG (Lac de Gras) joint venture with Dominion Diamond Corp. That project borders on the mineral leases where Diavik is located. Ekati is 40 kilometres to the northwest. Dominion plans to drill several targets later this summer as part of a $2.8-million exploration program. North Arrow will have a 30% interest in the JV.

With a target on its back, Dominion is highly motivated to enhance shareholder value. And that extends beyond mine operations to exploration and new discoveries. In May, Dominion announced a “renewed strategic focus on exploration” and a $50-million, five-year exploration budget.

A FANCY EDGE

As for Naujaat, North Arrow is revisiting the project after a polishing exercise yielded fancy yellow diamonds that turned some heads in the industry. Several were certified “fancy vivid” diamonds, a coveted designation in the coloured diamond world. The quality of the polished stones suggests the fancy orangey yellow diamonds at Naujaat are considerably more valuable than the June 2015 valuation of the roughs indicated.

The primary conclusion of the diamond evaluators was that the 384-carat parcel of Naujaat diamonds was too small to properly evaluate. North Arrow plans to remedy that, in part, by collecting a 200-tonne bulk sample that should yield another 80 to 100 carats. The sample will be taken from the kimberlite’s highest-grade zone, A61. Lab results are expected in early 2018.

Another complicating factor at Naujaat is the presence of two distinct diamond populations of different ages, including a population of rare fancy yellow diamonds. It’s a consideration that was not factored into the prior carat valuation. It will be next time. Diamonds are a rarity play, and diamonds that occur less frequently — such as coloured diamonds and large diamonds — are more valuable. Yellow diamonds made up only 9% of the 2015 Naujaat sample by stone count, but more than 21% by carat weight.

The drilling at Naujaat is targeting kimberlite between 200 and 300 metres in order to bring material designated target for future exploration (TFFE) into the Inferred category. That drilling, plus the mini bulk sample, should help North Arrow better evaluate the diamond deposit on the path to a future Preliminary Economic Assessment. The Q1-4 kimberlite has a horseshoe shape that makes it amenable to open-pit mining and a low strip ratio. A larger bulk sample is planned for 2018.

COLOURED CARATS

Fancy yellow diamonds were thrust into the spotlight earlier this month when Dominion unveiled the striking 30.54-carat Arctic Sun, a fancy vivid yellow diamond cut from a 65.93-carat stone unearthed at Ekati. Dominion also played up coloured diamonds in their latest corporate presentation — specifically, the sweetener effect of high-value fancy yellow and orange diamonds at Misery.

Dominion Diamond Corp.’s 30.54-carat Arctic Sun fancy yellow

The potential emergence of Canadian coloured diamonds could help solidify Canada’s position on the world diamond stage, according to analyst Zimnisky. On the branding and marketing side, Canadian diamonds continue to have strong appeal because of their high quality and ethical sourcing.

And the two recent Canadian mine openings are a bright spot for the global industry, despite early growing pains at both Gahcho Kue (lower-than-expected values) and Renard (breakage), he pointed out.

“There is absolutely an opportunity to sell Canadian diamonds at a premium, especially in North America,” Zimnisky said. The United States remains the world’s largest diamond market, despite the growth in demand from China and India.

Important hurdles remain before any mine is built at Naujaat, but the strength of North Arrow’s management team bodes well for success, according to Zimnisky.

“North Arrow is looking for something world-class and it’s high-risk, high-reward,” said Zimnisky, who has seen the company’s cut and polished fancy yellow diamonds: “They’re beautiful.”

The appetite for fancy yellow and other coloured diamonds remains strong, despite the closure or pending closure of two of the mines that produce many of them. Last year a De Beers store opened on Madison Avenue in New York, Zimnisky said, and the feature diamond on opening day was a very large fancy yellow of more than 100 carats.

DISCOVERY POTENTIAL

Further north of Naujaat on Nunavut’s Melville Peninsula is another North Arrow project with a good shot at a kimberlite discovery. At the Mel property, 210 kilometres north of Naujaat, North Arrow geologists have narrowed down and defined three kimberlite indicator mineral (KIM) trains through systematic soil sampling over several seasons. Last year’s till sampling defined where the KIM train is cut off, suggesting the bedrock kimberlite source is nearby.

The discovery of a new kimberlite field this season is possible, since kimberlites in the region outcrop at surface. “It’s a first look, but there’s potential for discovery without drilling,” says CEO Ken Armstrong.

As for the Lac de Gras joint venture, the US$1.1-billion hostile takeover bid for Dominion unveiled by the private Washington Corp. earlier this year may work in North Arrow’s favour. In addition to spurring a stock surge, the bid forced the diamond miner to crystallize its focus on creating shareholder value. And a key strategy for Dominion, with its two aging mines, is a renewed exploration push.

Finding new diamondiferous kimberlites in proximity to its existing operations would be a big boost for Dominion. One of its best shots is through the joint venture with North Arrow, which covers 147,200 hectares south of Ekati and Diavik. Dominion is spending $2.8 million on the project this season, including a planned drill program in the fall. North Arrow is well-positioned to capture the value of any Dominion kimberlite discoveries made.

North Arrow also plans to drill two or three promising kimberlite targets at its nearby 100% owned Loki project, dovetailing with the completion of the LDG drilling. The company has received a $170,000 grant from the Northwest Territories government to drill Loki. North Arrow will also conduct till sampling in the fall at Pikoo, its Saskatchewan diamond discovery, in advance of a potential early 2018 drill program.

Disclosure: Author owns shares of North Arrow Minerals. North Arrow is one of three company sponsors of Resource Opportunities, helping keep subscription prices low for the subscriber-supported newsletter. North Arrow Minerals is a high-risk junior exploration company. This article is for informational purposes only and all investors need to do their own research and due diligence.

Subscribe to Resource Opportunities until July 15 and use COUPON CODE JUNE to receive US$100 off regular subscription prices of $299 for 1 year and $449 for 2 years. Our focus is actionable investment ideas with high speculative upside potential. Recent examples: $ERD.T at 37.5c & $SBB.T at 39c. Join today and profit!

Their unique combination of portability and value make diamonds a favoured target of thieves, both on the big screen and in real life.

In The Pink Panther, a distinctive pink diamond was fodder for several movies worth of escapades between bumbling Inspector Clouseau and the elusive jewel thief.

Away from the screen, one of the biggest thefts was the Antwerp diamond heist of 2003. Thieves planned it for years, including posing as diamond merchants and renting office space in the Antwerp Diamond Center. They then made off with more than US$100 million in diamonds and jewelry from a heavily fortified safe. The bad guys were arrested; the gems were never found.

However, the greatest diamond heist of all time didn’t involve masked men, gunpoint or intricate plans concocted over several years. In fact, it didn’t involve coercion at all.

It went down rather quietly in the fall of 2009 when upstart Lucara Diamond Corp. bought a controlling interest in AK06, a De Beers diamond project in Botswana, for US$49 million. De Beers’ discovery of the nearby AK1 kimberlite — now Orapa, the world’s largest diamond mine — had launched a diamond district in Botswana’s Kalahari desert. But the diamond giant was now shedding assets and William Lamb, then Lucara’s only employee and now its CEO, was looking.

—

Subscribe to Resource Opportunities this month and use coupon code JUNE to receive $100 off regular subscription prices of $299 for 1 year and $449 for 2 years. That’s considerably less than the profit on one successful trade, making Resource Opportunities one of the best value propositions in the newsletter world. Our focus is actionable investment ideas with high speculative upside potential and compelling narratives on the sector’s strongest companies. Recent examples: $ERD.T at 37.5c & $SBB.T at 39c. Join us today and profit!

—

Lamb had been hired the previous year by Lukas Lundin, the Swedish tycoon whose international mining empire is based in Vancouver. The idea of a diamond company called Lucara was hatched earlier during a Lundin lunch with Catherine McLeod-Seltzer and Eira Thomas (who contributed the “ca” and “ra,” respectively, for the company name). Lamb spent more than a year scouring the globe for prospective diamond projects and plotted them on a spreadsheet, he told me during an interview in Botswana. AK06 made his short list.

He ironed out the purchase price for a 70% stake in AK06 during a 5-minute phone conversation with an executive at De Beers, where Lamb had worked for several years. Lucara later bought out JV partner African Diamonds — who couldn’t afford to fund their share of mine construction costs — to take control of 100% of the project. AK06, of course, became the Karowe mine, the source of many of the world’s largest and most valuable rough diamonds. Lucara has now sold 145 diamonds for more than US$1 million each, generating US$528 million.

Lucara sells its largest stones through Exceptional Stone Tenders, where buyers submit sealed bids over a number of days. On May 11 Lucara announced sales proceeds of US$54.8 million from its latest tender, the largest yet. The sale featured 15 diamonds for a total of 1,765 carats, including a 374-carat Type IIA diamond, below, that fetched US$17.54 million. The 374-carat stone broke off the 1,109-carat Lesedi La Rona, the world’s most famous diamond. It was purchased by Graff Diamonds, whose owner Laurence Graff is arguably the most powerful player in the global diamond trade. I suspect he desires the larger companion piece.

Graff Diamonds paid US$17.54 million for this 374-carat stone.

The “Lesedi La Rona” — “Our Light” in the local Tswana tongue — was unearthed in November 2015. It is the largest gem-quality diamond recovered in a century and the second largest ever. The stone was named last year in a contest open only to Botswana residents. Last year Lucara put the Lesedi up for live auction at Sotheby’s in London. But the diamond failed to sell because bids didn’t hit the reserve price. More on that later.

Lucara sold the 813-carat Constellation diamond, recovered at about the same time, for US$63 million — a record for a rough diamond — as well as a share of the profit generated from the cut stone. Notably, the price tag for the Constellation exceeded what Lucara had paid just seven years earlier for a controlling interest in the mine that produced it.

I travelled to Botswana recently to visit Lucara’s operations and learn more about both where the company has been and where it’s going. Also on the tour was the Africa correspondent for a Swedish daily newspaper and an analyst for Nordea, a large Swedish bank. There are plenty of reasons to be bullish Lucara and I have purchased more shares in the company since I returned.

“Big” and “beautiful” were recurring themes of the trip. After the site visit, I went on a two-day safari at a lodge on the Boteti — the only river that runs through the Kalahari Desert. Watching elephants, hippos, lions, giraffes and zebras in their natural habitat was an amazing experience. Fun fact: a group of zebras is called a “dazzle.”

BOTSWANA, DIAMOND POWERHOUSE

I flew into Gaborone, Botswana’s capital, through Frankfurt and Johannesburg. “Gabs,” as the city is known colloquially, has become a global diamond centre as Botswana has risen among the ranks of producers. The African nation is now the second largest producing nation by value, unearthing 22% of global supply, as outlined by New York-based diamond analyst Paul Zimnisky (Russia is first, Canada third). Most of the Botswana stones come from the Jwaneng and Orapa mines, located in the same neighbourhood as Karowe.

In 2013, De Beers moved its sorting and sales operations to Gaborone, an exclamation mark on Botswana’s emergence as a diamond power. Botswana owns the other 15% of De Beers not owned by Anglo American, as well as 50% of Debswana, a De Beers JV. Diamonds generate up to 50% of government revenues, funding universal health care and education (including post-secondary). Botswana is one of Africa’s fastest-growing economies and has a higher GDP per capita than South Africa.

One of the first stops for our small group was the gated Diamond Technology Park (DTP) on the outskirts of Gaborone. The compound is the headquarters for Lucara and other Botswana diamond miners. Down the street is the De Beers sorting centre. A helipad atop that building attests to former De Beers boss Nicky Oppenheimer’s fondness for helicopter transportation.