![]()

— FOR SUBSCRIBERS ONLY —

Momentum is Growing

By Lawrence Roulston

For several months we have been saying that the junior resource industry has bifurcated, with the majority of companies struggling for survival, while a few companies are on a solid path to recovery.

We have noted that astute investors have been evaluating the exceptional opportunities available in this depressed market and that billions of dollars of “smart money” is sitting on the sidelines, looking for a suitable entry point. For months, those investors have been quietly accumulating shares of high quality companies as they are dumped by investors looking to get out of resources.

The pace of activity has now ramped up in a dramatic way, as some of those investors have begun to deploy their money in a much more aggressive manner. In fact, many people will be surprised to learn just how much financing and takeover activity is now underway.

If asked to make an estimate, very few people would come close to guessing that over the past seven weeks, more than $1.3 billion of new financing has been injected into the junior resource companies.

That figure is the sum of the financing deals that have closed or which are secure and due to close very soon. It does not include the myriad of companies attempting unsuccessfully to raise money. (Dollar amounts in this article refer to United States dollars unless otherwise indicated.) That level of new financing is not far off the record level of financing that the industry enjoyed during the boom period from 2009 to 2011.

Clearly, a great many companies are still struggling to raise money. In fact the majority of companies and the majority of the players in the industry are facing a brick wall as they seek to raise new money, thereby perpetuating the popular notion that financing is still hard to come by. Yet, as we can see from the vast amount of money now flowing into the industry, some companies are able to raise all the money they need.

The new money is being spread across a range of companies, from early stage exploration through production. We don’t have all the details, but it appears evident that the new financing is coming from a small number of knowledgeable investors who are investing in carefully selected companies. Retail investors are still nowhere to be seen.

In the seven weeks from September 1, junior resource companies raised at least $749 million in equity and a further $623 million through debt or streaming. There were two large transactions on the equity side and two on the debt side, with the balance spread across a large number of transactions.

Fortress Minerals (FST.H), soon to be Lundin Gold (LUG.T), has successfully raised $200 million in equity and a further $39.5 million in debt to develop the Fruta Del Norte gold project in Ecuador, with the Lundin Family Trust subscribing for nearly $113 million of the offering. Mountain Province (MPV.V) was another standout on the equity side, raising C$100 million targeted to development of their diamond project in northern Canada. The balance of the new equity was spread across 64 transactions with an average ticket size of just over $7 million, ranging from under a million to $30 million earlier this month for a gold development project in Burkina Faso. The bulk of the money 65% – was raised in Canada, with Australian, US, Hong Kong and London listed companies making up the balance.

The companies that we cover in Resource Opportunities scored more than their fair share of the global financing total, raising $130 million over the past seven weeks, representing more than a third of the money raised in Canada.

Those companies are:

- NexGen: C$11.5 million;

- GoGold: C$20 million; (not closed yet)

- Millrock: C$4 million;

- Balmoral: C$12 million (C$10 million private placement and C$2 million warrant exercise);

- Falco Resources: C$10 million;

- TerraX: C$2.8 million;

- Virginia: C$70 million (this deal has not closed, but the money is committed and will close shortly).

The biggest recipient of new debt – $200 million – was Romarco Minerals (R-T), with the money going toward development of their Haile gold project in South Carolina. The next biggest debt deal was a $110 million debt facility awarded to MZI Resources for development of an industrial mineral project in Australia. A $50 million bridge loan was secured by Avanti Mining (AVT-TSXV) as that company continues to seek $800 million for development of a molybdenum project in northwestern British Columbia. In July Avanti signed a mandate letter with a syndicate of lenders with regard to a US$612 million debt facility.

Another 15 companies raised $207 million by way of straight debt or convertible debentures over the past six weeks. Arian Silver also secured $16 million by way of a base metal stream, an innovative financing approach that is just beginning to gain traction.

For the junior resource industry to raise $1.1 billion of new cash in a seven week period would be remarkable even in a booming market. To see that level of new financing at a time when the market is perceived as dead is truly an eye opening revelation.

The above figures apply only to the junior companies. Larger companies are also raising money at a torrid pace. For example, Chilean industrial minerals producer SQM raised US$250 million of new debt. Lundin Mining last month closed a US$1 billion debt financing. Earlier in the month, Lundin raised $674 million of new equity.

Mick Davis, who played a lead in building Xstrata, has secured equity of $4.8 billion for his new company, X2 Resources, with several billion dollars of debt to back that up. His aim is a repeat of his earlier successes, whereby he built huge mining companies. X2 is on the hunt for acquisitions.

Takeover activity is also heating up. The takeover of Cayden by mid-tier gold producer Agnico Eagle (AEM-T) is set to close before year end. Cayden shareholders are to receive 0.09 of an Agnico share for each Cayden. The deal, when first announced in September, was worth $205 million and represented a 42% premium over Cayden’s trading price.

There were at least eight other transactions initiated during that seven week period.

Copper producer Antofagasta offered C$96 million to acquire its joint venture partner Duluth Metals (DM-T). Duluth shares were trading at 12-14 Canadian cents for two weeks before the bid, and down to 7 cents the day before Antofagasta offered 45 cents a share. That bid price represents at 280% premium over the 20 day average price and was six-times higher than the last trade before the bid.

Antofagasta already owned 10% of the Duluth shares and 40% of the project. They certainly knew the value of the junior company and clearly thought it was a good buy, even at a huge premium to the trading price.

Newgold (NGD-T) bid C$0.21 for Bayfield Ventures (BYV-TSXV), a 50% premium to the trading price. Bayfield holds a property adjacent to a New Gold project in Ontario.

Kaizen Discovery (KZD-TSXV), which has a strategic funding alliance with Japan’s Itochu Corp, offered to buy a private British Columbia company with early stage exploration rights in Nunavut, northern Canada.

A Korean private equity firm offered to buy NMC Resource (NRC-TSXV) for C$.20 a share, a huge premium to the 4.5 cents that NMC had been trading at. NMC has a molybdenum exploration project in British Columbia.

A private investment group offered to buy Robust Resources, an Australia-listed explorer with projects in Indonesia, Philippines and Kyrgyz Republic. The offer, priced at 65% above the previous trading level, values Robust at A$50 million.

Orbis Gold, with several gold exploration and development projects in Burkina Faso, is fighting off an unfriendly offer from SEMAFO (SMF-T). The A$0.65 offer is 80% above the previous trading level and carries a total value of A$160 million.

Carlisle Goldfields (CGJ-T) is facing competing suitors. On November 11, Carlisle announced a private placement with AuRico that will give the mid-tier producer a 19.9% stake in the junior explorer. Carlisle is evaluating a Manitoba gold project. On November 13, another mid-tier gold producer – Nord Gold – offered to buy all of the shares of Carlisle for 9.6 Canadian cents. The junior was trading in a range of 2.5 to 4.5 cents per share before it caught the attention of the two gold producers.

Osisko Gold Royalties (OR-T) has offered to acquire Virginia Mines (VGQ-T) in a share swap that values Virginia at a 41% premium. The combined company will have a market value of C$1.3 billion.

In spite of the torrid pace of new financings and takeovers in the past few weeks, market sentiment remains extremely negative. We totally agree with the consensus that it will be some time yet before “the market” recovers for junior miners. In the meantime, investors who understand the cyclical nature of this industry, and are able to identify the worthwhile companies, are investing at a furious pace in the high quality companies.

Those investors who are getting in now, at the bottom of the market, will score huge gains as the resource market enters the next up-leg in the on-going cycle of ups and downs that characterizes resources.

The recent pace of investment activity could easily feed on itself and quickly spiral upwards. At this time, we suspect that the negative sentiment is still weighing on the market, moderating activity. Further, the coming year-end will break the momentum.

Once we are into the new year, sentiment could build quickly, as investors gain greater awareness that the smart investors are becoming quite aggressive and the bargains may not be around much longer.

Investors who wait for “the market” to turn will have to pay a lot more for the high quality companies. Or worse, they will buy the lesser quality companies thinking they are getting bargains.

Company updates

Falco Resources (FPC.V)

Falco reported impressive gold values from its on-going review of historic data at its Horne project in Quebec. Results include 9.2 meters at 31.5 grams per tonne and three meters at 42.7 g/t from historic drilling.

Falco holds a 100% interest in an extensive property position covering 70% of the entire Rouyn Noranda mining district. That property encompasses the Horne mine complex which was the backbone of major mining company Noranda from the 1920s to the 1970s. The property also hosts 13 other past producing mines.

Noranda was a base metal producer and with gold averaging less than $45 per ounce during the time that Horne was in production, there was no follow-up to the high-grade gold intercepts. Although copper was the primary focus for Noranda, this gold-rich base metals system also yielded 12 million ounces of byproduct gold, demonstrating the enormous gold potential of the district.

Falco is compiling, reviewing and digitizing results of 80 years of exploration work around the Horne complex, including 6400 drill holes. The recent work identified 16 distinct areas where historic drilling identified high-grade gold occurrences. None of those hits was followed up by Noranda. Earlier work by Falco identified 11 other gold zones.

Those newly found gold zones are outside of the resource estimate previously reported by Falco. (An inferred resource hosts 2.2 million ounces of gold in 25 million tonnes at 2.6 g/t gold, 0.23% copper and 0.7% zinc.) Those new gold zones have the potential to add ounces and to substantially boost the average grade of the resource.

There is an enormous amount of underground development already in place and a concentrator and a smelter located adjacent to the Falco property. With the development in place, and those facilities nearby, development of the Horne complex could be undertaken at a substantially lower capital cost than would be a case for a new mine development.

Beyond the Horne complex, the Falco geological team is also reviewing the exploration potential on the balance of the extensive property position. With 13 other past producing mines and 80 years of production and exploration history, the geologists have an exceptional starting position for an exploration program.

The extraordinary potential of the Rouyn Noranda district and the value of the Falco property and database attracted the attention of one of the most successful mine developers in the industry. Sean Roosen co-founded Osisko and led the effort to develop the Canadian Malartic gold mine, which is now producing 525,000 ounces per year. A bidding war earlier this year resulted in two gold producers jointly buying that mine for $3.9 billion. Mr. Roosen, who now heads a successor company to Osisko, has joined Falco as chairman and also made a substantial investment in the company.

While many exploration companies are starved for capital, Falco has just raised C$10 million with which to advance its exploration program. Falco plans an extensive six-month drilling program to follow-up on the newly identified gold zones. Exploration on the other parts of the property is also ongoing.

The potential for further big discoveries in a prolific district like Rouyn Noranda is readily apparent. The further endorsement of that potential, in the form of a big commitment from a highly knowledgeable industry expert, makes this a very appealing investment.

Price: $0.425

Shares Outstanding: 93.97M

Shares Fully Diluted: 107.22M

Market Cap: $40.4 M

Contact Investor Relations

(phone #1.855.238.4671)

http://www.falcores.com

Fortuna Silver (FVI.T)

Fortuna reported record revenues in the third quarter of $46 million. Its two mines in Mexico and Peru generated $17.8 million of operating cash and $7.8 million of net income. Silver production in the quarter was 1.8 million ounces, along with 9751 ounces of gold and 11 million pounds of lead and zinc.

Higher production at the San Jose mine in Mexico offset declines in metal prices, resulting in the gain in revenue. Reduced costs, higher grades and improved recoveries resulted in higher profit margins in spite of falling prices for silver and gold. Management is working to further reduce operating and corporate costs and to continue to improve operating efficiencies from the existing operations.

Fortuna is presently evaluating an expansion of the San Jose operation from the current 2000 tonnes per day to 3000 tpd. At that level, San Jose is expected to produce 7 million ounces of silver and 50,000 ounces of gold annually. Capital expenditure is estimated at $27 million, with full production expected by the third quarter of 2016.

Fortuna management has been shopping for acquisitions for some time, but so far has wisely held off as metal prices and share prices declined over the past year. The company is in an exceptionally strong financial position, with $72 million of cash and an un-drawn $40 million credit facility giving it flexibility for acquisitions and/or further organic growth.

Investors appreciate how well this company is performing, rewarding it with a share price that is 60% higher than at the start of the year. With further operating improvements in sight and another big boost to the production level expected in the next couple of years, the share price is likely to continue that upward trend.

Price: $5.57

Shares Outstanding: 127.15 M

Shares Fully Diluted: 131.5 M

Market Cap: $658.6 M

Contact Investor Relations

(phone #1.604.484.4085)

http://www.fortunasilver.com/

Virginia Mines (OR.T)

Virginia has received a takeover offer from Osisko Gold Royalties (OR-T). The offer of 0.92 Osisko share for each Virginia share represents a 41% premium to the trading price of Virginia prior to the offer. The merger will create a leading mid-tier gold royalty company with a market value of about C$1.3 billion.

Virginia holds a 2.2% royalty on the Eleonore gold mine in Quebec, which is just beginning to produce gold. Goldcorp purchased the Eleonore project from a predecessor company to Virginia in 2006 for $420 million, leaving the present company with the royalty, cash and an extensive exploration portfolio. Goldcorp has now developed the mine, which is in production with a plan to ramp up to 600,000 ounces per year by 2018.

The Virginia management and exploration team, which has already generated enormous value for shareholders, will be an important part of the new company. Virginia’s CEO Andre Gaumond will become a senior vice president and the geological team will continue the exploration efforts that have already made a number of gold and base metal discoveries.

A predecessor company to Osisko Gold Royalties developed the Canadian Malartic gold mine, which is now producing 525,000 ounces per year. Earlier this year, gold producers Agnico Eagle and Yamana beat Goldcorp in a bidding war to purchase the Canadian Malartic mine for $3.9 Billion. The deal left Osisko Gold Royalties with cash, a 5% royalty and an extensive portfolio of exploration properties.

Sean Roosen, who led the development of the mine and now leads Osisko will be the CEO of the combined company. This new company will have C$270 million of cash (C$200 million from cash on hand plus a further C$70 million from a private placement done as part of the deal). At full production, the two royalties will yield the company about 40,000 ounces per year, at minimal cost.

Bringing together two highly successful management and geological teams sets up the new company for further gains in shareholder value: from exploration success as well as growth through further acquisitions. It will also benefit from increases in the gold price.

The two high quality gold royalties and the cash on hand provide a solid basis of value for a company that has enormous growth potential. New Osisko will itself be a tantalizing takeover target for the larger gold royalty companies, which are struggling to find large, high quality royalties. A bid from Franco-Nevada or Royal Gold is likely within months, providing another near term boost in value for shareholders.

Price: $14.34

Shares Outstanding: 83.6 M

Shares Fully Diluted: 83.6 M

Market Cap: $1.2 B

Contact Investor Relations

(phone # 416.363.8653)

http://www.osiskogr.com

Zephyr Minerals (ZFR.V)

Zephyr is advancing its high-grade gold deposit in Colorado. A bulk sample taken from the deposit is presently being tested to confirm the metallurgy. Results will be used to develop the recovery plant design and to optimize the process.

Previous studies have shown 90% recovery of the gold through gravity and froth flotation. The present program aims to further improve on that recovery rate. The company is also carrying out environmental monitoring as part of the permitting process. Results of the present work will support a preliminary economic assessment (PEA).

The deposit, as presently outlined, is small but with an exceptionally high grade. An inferred resource of 392,000 tonnes hosts 132,000 ounces at a grade of 10.5 grams per tonne. The independent resource report notes that the two zones comprising the resource have good potential for delineation of further resources.

Beyond the two zones in the resource estimate, there is additional potential in other zones. For example, a historic estimate for the Windy Point zone outlined 15,800 ounces grading 12.3 g/t, but further work is required to verify that estimate. There is also gold in the Copper King zone, but it has not yet been delineated. Other gold bearing zones have been identified on the property, providing potential for further discoveries.

The Dawson property is in a region with a long mining history and is readily accessible. The deposit could be developed fairly quickly (18 months or less) and at a modest capital cost (in the order of $25 million).

Zephyr had almost no cash at the end of June, but has since raised C$260,000 in a private placement priced at C$0.15. That seems a small amount of money with which to advance a project of this nature, but this management team can get a tremendous amount accomplished with that amount of money. Management salaries total just C$16,000 a quarter, leaving the balance to fund the studies needed to advance the project. They plan to have a PEA completed before they need further funding. That study should support a higher share price.

The management team are experienced and highly professional, more than capable of developing this project. The high-grade of the gold, the great location and the modest capital requirements make it a favorable project for which to secure funding.

A number of small gold producers would see this as a very attractive development project. Completion of the PEA will give those companies the information they need to properly assess the project.

Price: $0.16

Shares Outstanding: 22.58 M

Shares Fully Diluted: 25.42 M

Market Cap: $3.6 M

Contact Investor Relations

(phone #1.902.446.4189)

http://www.zephyrminerals.com

Cayden Resources (CYD.V)

The acquisition of Cayden by mid-tier gold producer Agnico Eagle (AEM-T) is set to close before year end. Cayden shareholders are to receive 0.09 of an Agnico share for each Cayden. The deal, when first announced in September, was worth $205 million and represented a 42% premium over Cayden’s trading price. The decline in the gold price and shares of gold companies across the board has lowered the value to be received by Cayden shareholders, but this still represents an attractive offer.

Agnico is forecasting production next year of 1.6 million ounces of gold from four mines in Canada, one in Finland and three in Mexico. The company is well managed and has grown steadily over the past few years, with further organic growth underway. It is profitable, with cash and a manageable debt level and access to further debt to fund further mine development.

True Gold Mining (TGM.V)

True Gold is continuing development of its Karma gold mine in Burkina Faso, with first gold production still on track for late next year. Investors in True Gold were unnerved last month by a civil uprising that saw the president resign following angry protests.

After serving as president for 27 years, having taken power in a coup and winning four disputed elections, Blaise Compaore proposed to change the constitution to allow him to run in yet another election. That was too much for the people, who spilled into the streets a million strong.

In order to avert further violence, the military stepped in and encouraged him to resign.

The military first seized power, but after pressure from the African Union and others, and under pressure from ongoing protests, a civilian president with broad popular backing has now been sworn in for a 12 month term. The recent events, rather than a chaotic episode, were more a democratic process at work as the people spoke out to remove a corrupt leader. The interim government has set a timeline for elections within a year. Burkina Faso is generally a peaceful country, with a fairly homogenous population and little racial or sectarian strife.

As we anticipated last month, the turmoil generated a buying opportunity for a company on track to begin production at the end of 2015.

Price: $0.25

Shares Outstanding: 398.4 M

Shares Fully Diluted: 482.9 M

Market Cap: $105.6 M

Contact Investor Relations

(phone # 604-801-5020)

www.truegoldmining.com

NexGen Energy (NXE.v)

Since we last wrote about NexGen, the company released one of the most impressive uranium intercepts ever drilled in the Athabasca Basin. The market knew drill hole AR-14-30 was going to be good based on the pre-released scintillometer results, but even those results underestimated the strength and continuity of mineralization at the Arrow discovery.

The highlight intercept was 63.50 metres at 7.54% U3O8 including 46 metres at 10.32% U3O* and 20 metres of 10.17% U3O8. The drill hole was the company’s first ever vertically drilled hole and based on a 0.05% U3O8 cut-off, the composite grade thickness (GT) measured at 908.81 putting it in the top 3 uranium drill holes in the Basin.

Despite this outstanding result, shares actually fell the day the results were pre-released, closing down $0.025 to finish at $0.385 per share. The following day, NexGen announced a $10 million bought deal financing of flow through shares (no warrants) at $0.46 per share, representing a 19.5% premium to the previous day’s closing price.

The company eventually closed the $11.5 million, expanded financing on November 12.

NexGen is now well-financed to aggressively drill this winter. The majority of the drilling will likely be at the Arrow discovery in order to try and define just how big the area of mineralization is which currently stands at 515 by 215 metres. There are also some lake based targets that may be drilled while the lakes are frozen as well as some other regional targets.

Given that their 18,500 metre summer program only cost them an estimated $7.5 million, the company has enough cash to drill at least another two programs of that size.

Additionally, there are 4.4 million warrants expiring at $0.50 in mid-January and an additional 7.1 million at $0.55 at the end of February. If exercised, these warrants could bring in another +$6 million to the treasury.

Price: $0.42

Shares Outstanding: 196 M

Shares Fully Diluted: 249 M

Market Cap: $82 M

Cash: $15 million

Contact: Kin Communications

(604 -684-6730 )

www.nexgenenergy.ca

Charts of interest

After getting trounced during the last week of October and testing the 2008 lows the senior gold miners are now in the fourth week of a rally which has seen the GDX reverse all of the losses incurred during the week of October 27th:

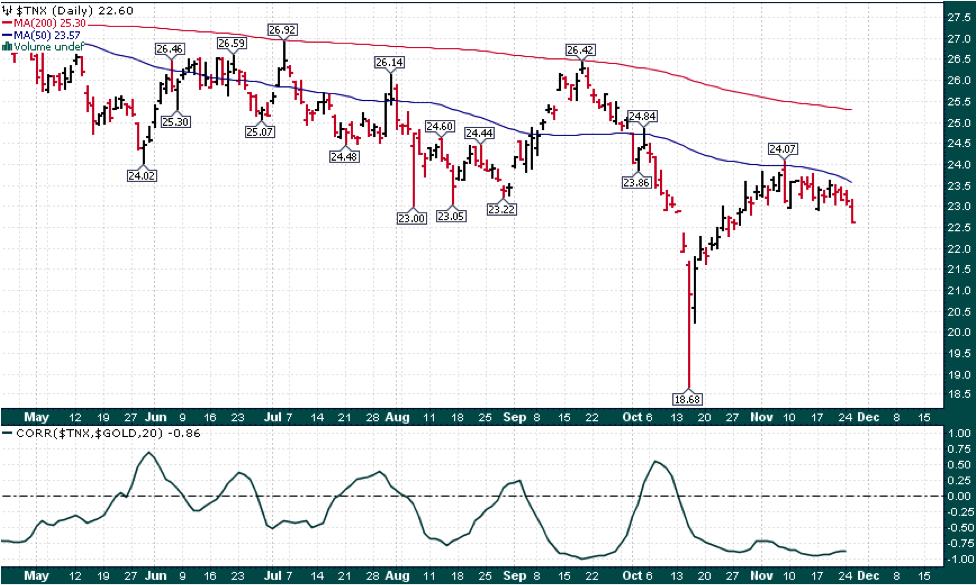

After bouncing back to test the falling 50-day simple moving average, 10-year note yields are beginning to roll over and head lower:

Yields have generally held a negative correlation to precious metals (falling yields mean higher precious metals prices and vice versa) as can be seen at the bottom of the above chart (86% inverse correlation).

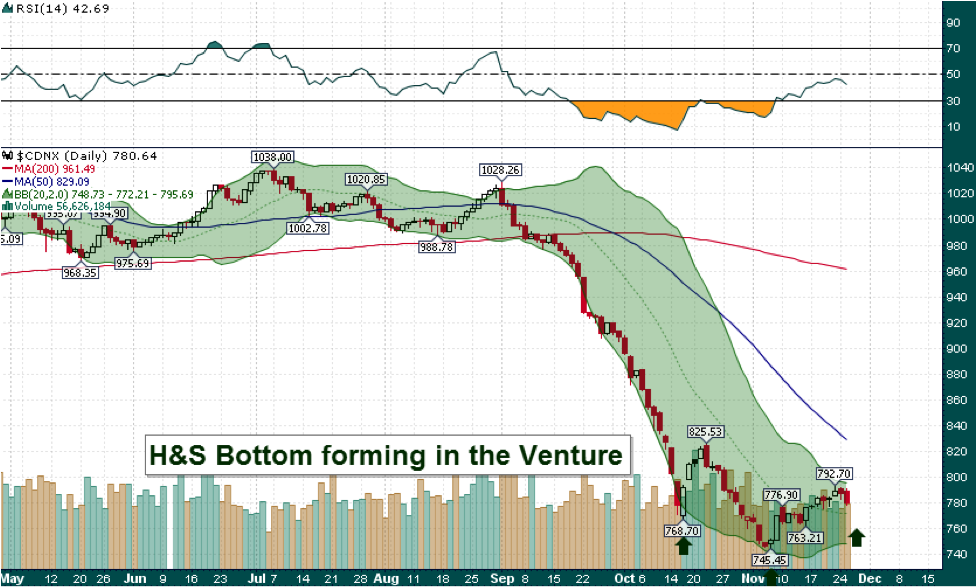

Meanwhile the TSX Venture Composite is forming a head & shoulders bottom pattern:

A further 1-2% during the next 1-2 weeks would set up the head & shoulders bottom pattern nicely and also fit well with our end of year tax-loss selling thesis: Tax-loss selling 2014: why this time is different. We would then be looking for a minimum 15-20% rally to kick off the new year.

After bottoming 3 weeks ago, gold continues to consolidate near $1200 just below the falling 50-day simple moving average:

As we pointed out on CEO.CA over the weekend, gold is in a very bullish seasonal period until the end of the first week of December. It is interesting to note that $1204.80 was the official 2013 year end closing price for gold.

Editorial Policy, Disclaimer and Disclosure: Resource Opportunities is written, edited and published by Tommy Humphreys, 602-1228 Homer St., Vancouver, BC, V6B 2Y5. Tel: (604) 697-0026 www.ResourceOpportunities.com

Editorial Policy: Companies are selected for presentation in this publication strictly on the merits of the company. No fee is charged to the company for inclusion. Currencies: Dollar and $ refer to US dollars, unless stated otherwise or obvious from the context (for example, a share price on a Canadian exchange). Readers are advised that the material contained herein is solely for information purposes. Readers are encouraged to conduct their own research and due diligence, and/or obtain professional advice. Nothing contained herein constitutes a representation by the publisher, nor a solicitation for the purchase or sale of securities. The information contained herein is based on sources which the publisher believes to be reliable, but is not guaranteed to be accurate, and does not purport to be a complete statement or summary of the available data. Any opinions expressed are subject to change without notice. The owner, editor, writer and publisher and their associates are not responsible for errors or omissions. They may from time to time have a position in the securities of the companies mentioned herein, and may change their positions without notice. (Any significant positions will be disclosed explicitly.) Author is not a registered investment advisor and this is not a formal investment recommendation. We are not telling you to go buy or sell this stock. We are telling you that we bought this stock and that we highly recommend that you research the stock to see if it is a good fit in a well-diversified portfolio. We recommend that you do as much research as possible on every stock you purchase or sell prior to any action. We recommend that you consult your investment advisor or broker prior to any action. We are not liable for any transactions you make after reading this article. Do your own due diligence prior to making any investment decision. Additionally, we invest with a 12 month or longer time horizon. If your time horizon is shorter, you may consider other investments.

Copyright: This publication may not be reproduced in whole or in part, in any form, without the express permission of the publisher. Permission is given to extract parts of the report for inclusion or review in other publications only if credit is given, including the name and address of the publisher.

James Kwantes is the editor of Resource Opportunities, a subscriber supported junior mining investment publication. Mr. Kwantes has two decades of journalism experience and was the mining reporter at the Vancouver Sun. Twitter:

James Kwantes is the editor of Resource Opportunities, a subscriber supported junior mining investment publication. Mr. Kwantes has two decades of journalism experience and was the mining reporter at the Vancouver Sun. Twitter:  Resource Opportunities (R.O.) is an investment newsletter founded by geologist Lawrence Roulston in 1998. The publication focuses on identifying early stage mining and energy companies with the potential for outsized returns, and the R.O. team has identified over 30 companies that went on to increase in value by at least 500%. Professional investors, corporate managers, brokers and retail investors subscribe to R.O. and receive a minimum of 20 issues per year. Twitter:

Resource Opportunities (R.O.) is an investment newsletter founded by geologist Lawrence Roulston in 1998. The publication focuses on identifying early stage mining and energy companies with the potential for outsized returns, and the R.O. team has identified over 30 companies that went on to increase in value by at least 500%. Professional investors, corporate managers, brokers and retail investors subscribe to R.O. and receive a minimum of 20 issues per year. Twitter: